TTF Group - Analysis of the Leading French Barrel Producer (Wine & Whisky)

A 71% family-owned business in a cyclical industry, currently feeling the pain (-40%) of the alcoholic beverage industry.

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

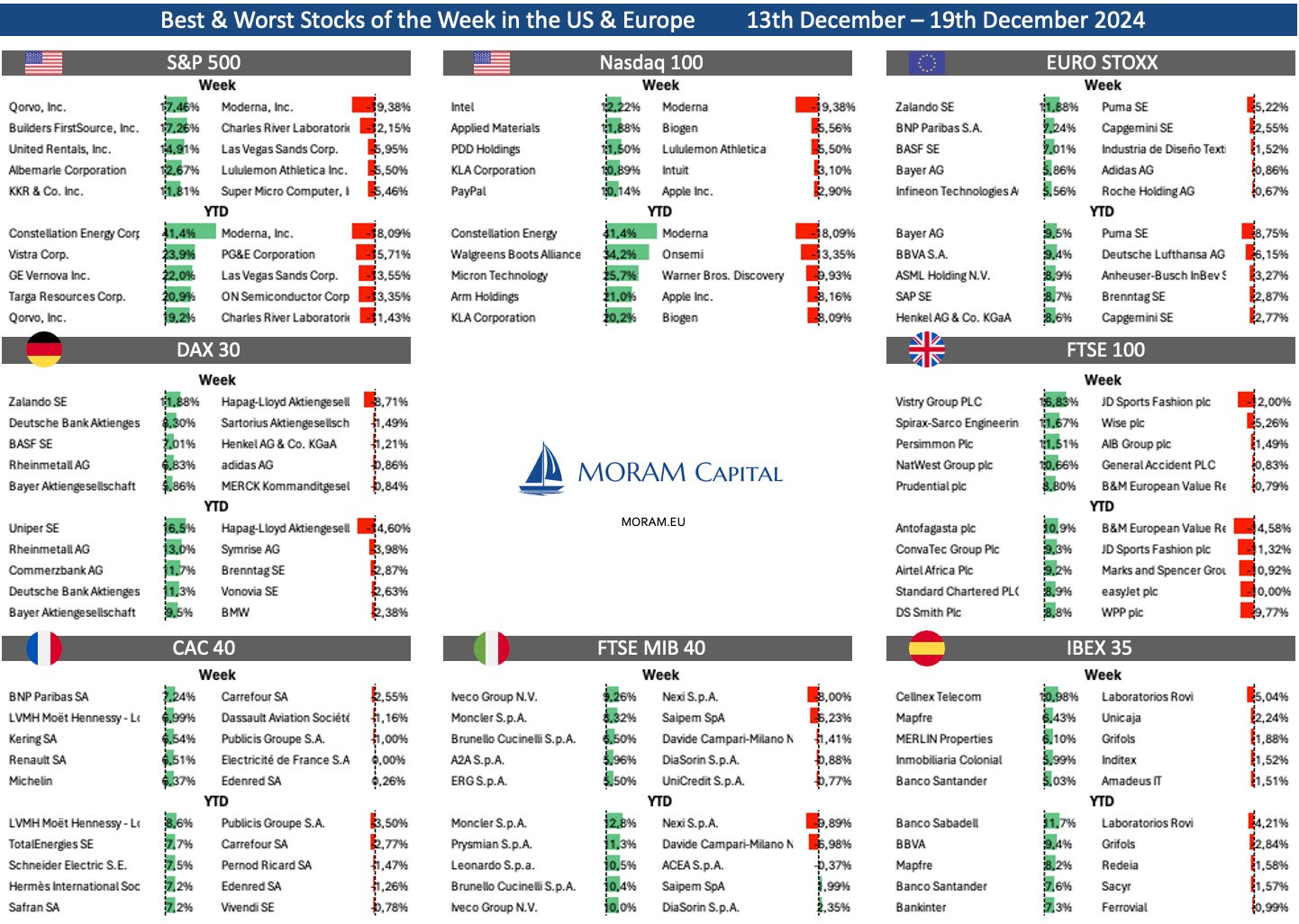

The Week in the Markets

Our weekly summary with the best charts & explanations to understand what happened in the markets this week in 5 minutes

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

TFF Group - During the last 2 months, we have been analyzing TFF Group, a leading manufacturer of barrels and oak casks for the wine and spirits industries. It is a French family-owned business (71% ownership) that holds a dominant position in all the segments they operate in and has experienced enormous growth in recent years (as well as M&A and investment in growth).

Over the past year, it has fallen by more than 40% due to the bullwhip effect stemming from reduced beverage demand and end-customer inventory accumulation (existing issues in the alcoholic beverage industry), and we believe this is the perfect time to present an in-depth analysis.

Ecoener - Thesis Update - Renewable energy company that is performing very well and is about to increase its operating assets by 75%). In this update, we review the current situation and update the financial model with electricity prices and the status of the parks under construction.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Investor Resources

Financial model Updates: Ecoener, Solaria, Vysarn, The Italian Sea Group, Catana

Data Center

Nota: Toda esta publicación está disponible en Español en nuestra web

The Week in the Markets

Summary

A tremendous week for the stock markets, fueled by the U.S. CPI data on Wednesday. It’s amazing how market sentiment can shift by a single decimal point… As often happens in weeks like this, small caps significantly outperformed the Mag7 (dragged down by Apple and its sales in China).

We highlight the strong start to the year for the European stock market, which is being boosted by a very weak euro, with Italy standing out (a country where we have been very active for several years, and its companies make up a significant percentage of our investment theses).

By sectors, Energy (with oil prices up more than 8% since the start of the year), Materials, and Financials (with excellent earnings results in the first week of earnings season) have led this week. On the opposite side, the Healthcaresector (heavily impacted by Eli Lilly, down 9%, which dropped 8% on Tuesday after Q4 sales forecasts for its weight-loss drug Zepbound came in below expectations) struggled.

Another winner this week has been Bitcoin, mainly driven by the potential intention of Trump (whose presidency begins this week) to announce a strategic Bitcoin reserve. As an anecdote? The cryptocurrency $TRUMP surged over 5000% in 24h since its launch surpassing $10 billion early Saturday morning.

Zooming in on styles, Momentum continues to lead (after an incredible 2024), and Private Equity funds have started the year strong after two very tough years.

Of the few that ended the week in the red, VIX (completely logical, being the so-called "fear indicator") closed the week below $16, along with the Japanese Nikkei and bonds, which retreated (as expected, moving with a significant correlation to the market’s interest rate cut forecasts) after two weeks of upward movement.

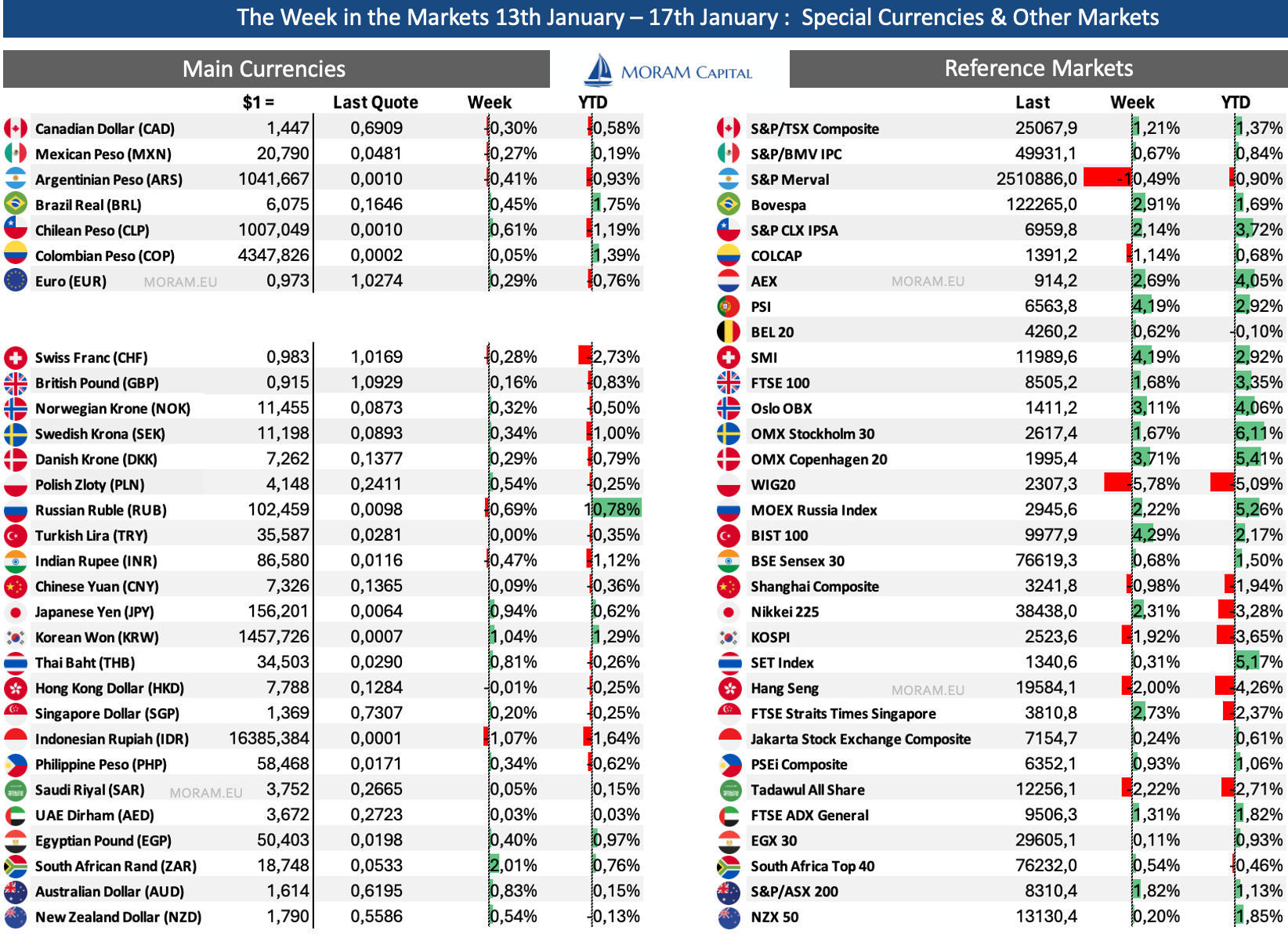

The Dollar maintains its strength (as you can see in detail in our new One-pager on Currencies & other indices, launched this week in the section "Interesting Data about markets this week & YTD").

We hope these new modifications to this section are useful, and we will continue iterating and improving with your feedback. Our goal is to provide the most comprehensive summary possible so that any investor can quickly review what happened in the markets this week in 5 minutes.

Macro highlights

US CPI

The December CPI report reflects a mixed inflationary landscape in the U.S., with upward pressure in goods and a slight deceleration in services.

Headline inflation rose 0.39% MoM, the largest increase since March, exceeding both November’s 0.31% and the expected 0.3%. On an annual basis, the rate climbed to 2.9%, marking the third consecutive increase, in line with market expectations.

Core inflation, which excludes volatile items like food and energy, increased by 0.23% monthly, below the forecasted 0.3%, and its annual rate eased slightly to 3.24% from 3.3%.

Goods inflation showed a rebound, driven by energy prices, with gasoline surging 4.4% in December (And watch out because the recent increases in the price of oil barrels are going to drive this component even higher in the coming months) Deflation in goods has nearly disappeared on an annual basis.

Services inflation moderated to 4.4% annually, down from 4.6%, largely due to slower increases in housing costs (4.6% vs. 4.7%). However, transportation services accelerated to 7.3% annually.

SuperCore index (services excluding housing) rose 0.28% MoM, bringing its annual rate down to 4.17%.

And translated to the market, it means that everything is no longer as clear as last week (only one rate cut in 2025). It’s amazing how much one decimal changes everything and the twists and turns that come from it. But these are the current rules of the game, and you have to understand them because they determine market sentiment.

Retail Sales

U.S. retail sales data for December were mixed, with a 0.4% monthly increase—the smallest in four months—below forecasts of 0.6%. Gains were led by miscellaneous retailers (+4.3%) and sports goods (+2.6%), while declines were seen in building materials (-2%) and food services (-0.3%).

Core sales, used for GDP calculation, rose 0.7%, the largest gain in three months.

Europe

Germany: German GDP fell by 0.2% after a 0.3% decline in 2023. The main cause was a lack of investment (the services sector grew by 0.8%). These figures come just weeks ahead of the country’s crucial snap election, which is expected to boost Germany’s competitiveness and reduce the uncertainty of recent months.

Eurozone: The next ECB meeting is on January 30, and after the minutes of the December meeting published this week, another 25 bps rate cut to 2.75% is anticipated.

UK: CPI unexpectedly eased to 2.5% in December (down from 2.6% in November). This strengthens market expectations that the BoE will lower interest rates in February. Meanwhile, GDP saw a modest increase of just 0.1% in November.

Interesting Data about markets this week & YTD

Earning Season 1Q25

This week, earnings season kicked off (mainly in the banking sector) with very strong results. In fact, the financial sector has been one of the main winners of the week, even though the CPI data should, in theory, have rotated flows from this sector to others. JPMorgan +8%, Citibank +12%, Blackstone +10%, Wells Fargo +10%.

Consensus forecasts for 4Q24 EPS show growth of +11.7%. Specifically, EPS for the Mag 7 is expected to grow by +22%, while EPS for the other 493 companies in the index is expected to grow by +8.7%.

This coming week, Netflix reports among the Mag 7. On our end, we will mainly focus on the recreational vehicles sector, where we have been active on the short side in the recent past but currently have no exposure. (This week, dealer MarineMax reports and usually provides a general overview of what to expect over the next 15 days with the rest of the companies in the industry.)

Remember that Monday will be a holiday on Wall Street due to Martin Luther King Jr. Day.

Tonnellerie Francois Frères - Equity Research

Introduction to Tonnellerie Francois Frères

Tonnellerie Francois Frères (TFF) is a family-owned (71% ownership) dry material supplier in the alcoholic beverage industry, they supply casks and barrels for wine and Scotch and Bourbon whiskies (Wine is 43% of sales and Alcohol 57%). The oak barrels are the key value adding component to these beverages (flavor, aroma and body sources) and the quality of the barrel determines the quality of the beverage to a large extent (this is a very simplified overview).

TFF has a dominant position in all the segments they operate, their market share is 25% in wine, 80% in Scotch whisky and 18% in Bourbon. The Wine segment operates worldwide, while the Alcohol segments operate in their geographical denominations (US Midwest & East and Scotland).

Since 2016, TFF Group has enjoyed a staggering growth thanks to the excellent execution of the Bourbon Division (39% Revenue CAGR over the last 7 years). TFF’s investments are ongoing, with the goal of increasing the current Bourbon capacity by 85% over the next 2 years.

Nevertheless, the current situation is quite different. TFF has suffered a 41% drawdown during the last year (main reason we started to analyse in deep the company two months ago, as we were already familiar with the quality of its business) as TFF is suffering the reduced consumer demand and the inventory accumulation impact from the beverage makers and distributors. But unlike other players of the value chain, this impact on TFF’s economics has a lag (it takes longer for them to reflect the market demand) due to:

The product of TFF is used for long beverage maturing cycles (can last for more than 10 years in some whiskies)

The barrels is consumed further downstream in the beverage supply chain than the product of beverage makers or glass/cork manufacturers.

After the Q2 Earnings release last week, the company is trading at COVID lows. It is unusual to see such a compounder business with still runway for growth and a strong moat provide a good entry point. It is a moment of uncertainty for the beverage industry: the looming tariffs, the recent negative press around alcohol, the macro consumer trends and the noise of climate change potentially impacting the last couple of poor wine harvests…We analyze in depth each of these points.

There are many dynamics playing out in this company, and this week, we are sharing an analysis with all the attention to detail it deserves. We touch on:

The beverage industry supply chain dynamics

Business model of TFF and its detailed operations

Breakdown of each one of the segments and the analysis of their macro and micro forecasts

Analysis of its Capital Structure (Debt, Working Capital…), Capital Allocation, M&A, Management…

Economics & Valuation including our downloadable spreadsheet

A detailed risk analysis that matches the significance of the company's situation

Our Conclusion about the opportunity on TFF

An extremely detailed analysis that explains the workings of the industry and examines the potential entry opportunity in a company in a highly compelling situation. Hope you find it interesting

The TFF Business

Before we delve into the specifics of each one of the beverages, it is worth explaining that, overall, the barrel and cask demand are result of various factors:

Bourbon, scotch and wine consumption volumes and regulations: Different categories may require multi-barrel ageing or longer ageing. Government regulations around the requirements of Bourbon and Scotch, minimum alcohol % content in beverages that can be sold in grocery stores and tariffs, are some external factors that impact volume, beyond overall consumption trends.

Inventories at their clients: Orders at their clients are subject to large YoY variations. Due to the multi-year period of ageing in some products, long-term forecasts guide the orders from their clients. These long-term forecasts are noisy and inaccurate, as predicting long-term beverage trends is not an easy task.

Harvest quality: To a large extent, the better the grape harvest, the larger the produced wine volume. Good harvests deplete inventories at their clients faster, while bad harvests reduce the order intake.

Availability of Bourbon barrels for scotch production: Scotch whisky is made with used Bourbon barrels.

Beverage Industry: Supply Chain

TFF Group is a supplier of the wet material processors in the beverage industry. Their clients are whisky makers like Diageo & Pernod and wine markers like our dear Italian Wine Brands. There are no pure publicly traded comparables to TFF. Other publicly traded companies that compete with TFF, only have barrel-making as a fraction of their revenues, such as Oeneo and Anora.

Ageing of the beverage inside the barrel:

The ageing of the beverage inside the barrel is the process that plays the most value-adding role amongst all the processes in the supply chain. Ageing inside the barrel is the main source of flavor, aroma and body.

It is interesting to understand the dynamics that play out during the ageing process: When it comes to the age of the barrel, think of it like a tea bag. The first time you use a tea bag, your tea has a lot of flavor. But when you use the same bag for a second cup of tea, it has considerably less flavor. It’s the same deal with a wine barrel. When a winemaker first uses a barrel, they usually get about 50% of the extract into the wine. On the second use, it goes down to 25% and diminishes even further after that. The same mechanism repeats with whiskies.

At the same time, the bigger the oak surface area/wine volume ratio during ageing, the stronger the influence of the oak and the faster the ageing process happens. In other words, smaller barrels have more of an impact on wine than larger barrels.

The Manufacturing process

High-level the barrel-making process has five steps:

Purchasing the wood: The supply dynamics differ depending on the geography. In France, 90-95% of the wood is purchased directly from the national forest authority. The government manages the stock of trees (oaks) better than private owners. Private companies do not always take proper care of their forests. They are not consistent in the offer (quantity and quality). It is difficult to manage tree inventory; It takes 250 years to have the oak ready. The government cuts the supply of wood to keep prices stable. That's fine with for TFF, as long as TFF can find the wood needed at acceptable prices. A drop in lumber prices is not the direction of this market in the long term. Supply is limited, impacted by climate change. Prices will tend to rise.

There is currently a good access to French wood. The process to acquire wood in France is transparent (no corruption). The wood goes to the player who pays the most for it. TFF pays handsomely, but they reflect their costs in their selling prices. France is in a very good situation as far as wood supply is concerned. It is possible to sign long-term contracts with the national forest authority, but only for sawmills. For this reason, TFF recently purchased 2 sawmills.

In the USA, the dynamics are different compared to France. TFF buys mainly from private suppliers. There is a market price for wood. The price of wood depends on all the uses that are given to wood in the economy (e.g. construction, flooring, furniture). Prices are stabilizing and even falling. This might result in lower price of barrels. Especially in the US due to its diverse climate, the origin of the wood matters.