Updates on Campari, Fortress Infrastructure, Excelerate Energy, Good Times Restaurants, ..

Updates after 1Q25 results

Hi There!

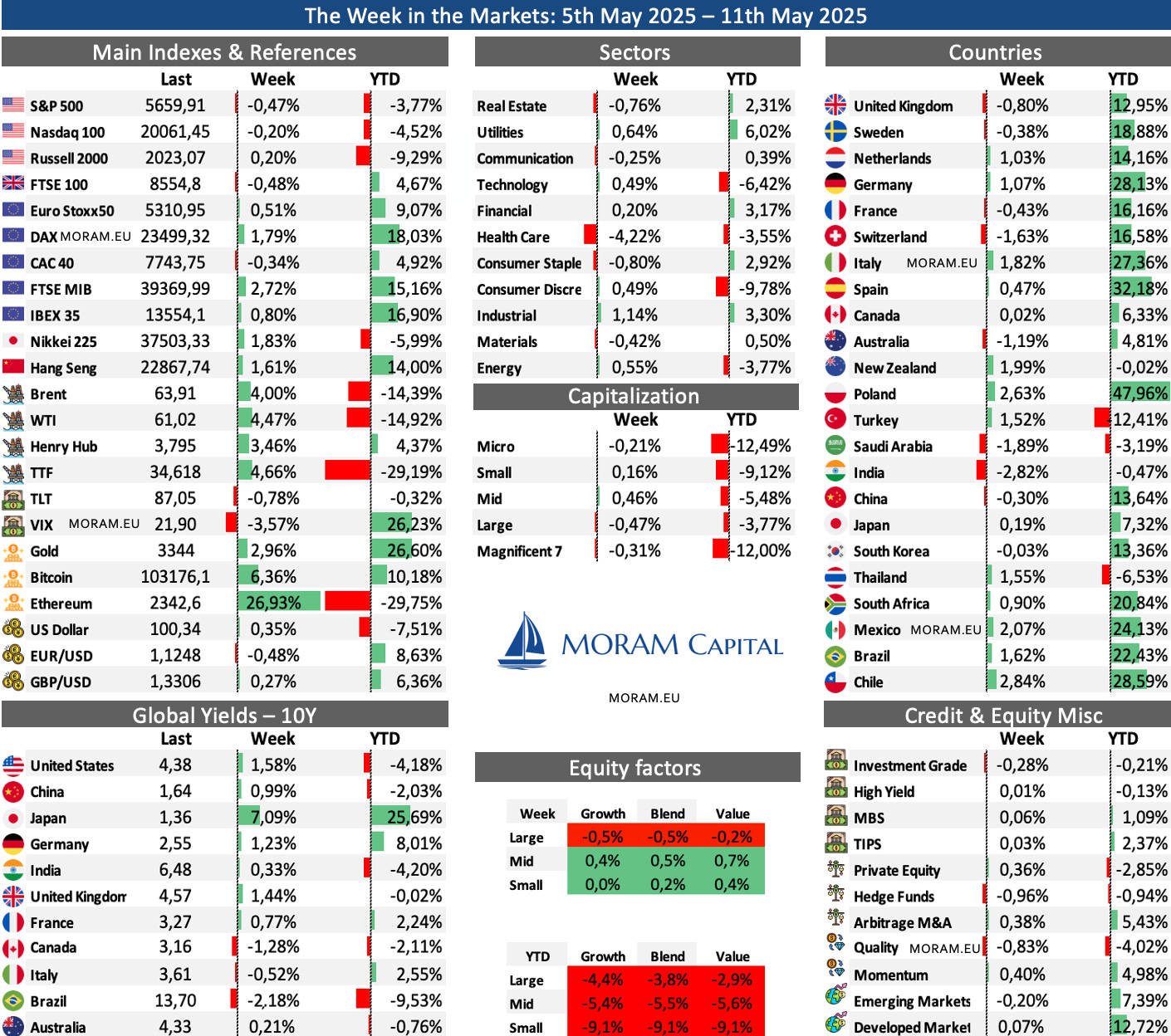

This week, we weren’t able to include the “The Week in the Markets” section due to the exceptionally high number of companies in our coverage universe reporting. However, we’re sharing our summary table and the key earnings to watch next week.

Equity Research (1Q25 results analysis & updates)

Fortress Infrastructure $ FIP

Campari $ CPR.MI

Excelerate Energy $ EE

Good Times Restaurants $ GTIM

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

This coming week

This week, apart from having news about the negotiations taking place this weekend between China and the United States in Switzerland (where, at first glance, positions are converging, and it is most likely that we will see a reduction in current tariffs — the 145% tariff is nonsensical, and we are seeing that containers continue to flow from China to the US), we will have the publication of the April CPI. And honestly, if the tension with the tariffs eases (we understand that they will remain for all countries, but close to the 10% that was ratified this week with the UK), and the CPI continues its downward trend, Powell should run out of reasons not to lower rates in July.

1Q25 Earnings Season

Within our universe of companies, the following are reporting:

The Italian Sea Group - 12th May

Newlat - 12th May

New Fortress Energy - 12th May

Ferretti - 12th May

Jack in the Box - 14th May

Arcos Dorados - 14th May

Epsilon Energy - 14th May

Sanlorenzo - 15th May

This coming weekend, we will do a special on Superyachts, focusing on the situation of Sanlorenzo, The Italian Sea Group, and Ferretti (with additional comments on the French companies). During the week, we will publish about New Fortress Energy if we find that the call provides meaningful insights. Similarly, we are planning to release a special on AutoPartner and Valaris, which posted very strong results and sold jackups this week at very good prices (we believe it is extremely undervalued, but the macro and oil situation isn’t supportive, for now).

Special Update - Fortress Infrastructure $ FIP

Fortress Infrastructure ($FIP) is an energy infrastructure company born from the spin-off of its parent company, FTAI, in the summer of 2022, separating the Transport & Aviation Parts business from the Infrastructure business.

FIP’s business focuses on acquiring, developing, and operating critical energy infrastructure assets in the United States. Specifically, FIP owns four assets and has several minority investments.

As a reminder (you have the full analysis here):

Transtar, a railroad business with stable annual growth of 10–15%, acquired in July 2021, is the company’s main driver with nearly $100MM in EBITDA.

Long Ridge, a 505MW Power & Gas plant (with a 20MW upgrade in progress) located in Ohio, of which FIP acquired the 50% it didn’t already own this past February 27th.

Jefferson operates Gulf Coast port infrastructure, with a main terminal for liquid hydrocarbons and a South Terminal focused on chemicals like ammonia. It’s expanding under a 15-year blue ammonia contract and owns key logistics assets like 299 tank cars and pipeline rights.

Repauno, a New Jersey port and logistics hub focused on liquid fuels, with Phase I operational and expansion underway. Phase II, set for late 2026, is expected to add $70M in AEBITDA via secured contracts, with financing anticipated in 2Q25. Phase III is in early planning and could add ~$100M of EBITDA longer term.

Since going public, FIP has been completing the construction and ramp-up of its other assets, securing long-term stable contracts. It now expects to triple its EBITDA in the next 18 months to over $350MM while carrying out multiple financing cost reduction efforts (its current financing ranges from non-tax bonds at 1.99% to preferreds at 14%, which it is trying to eliminate).

Today, after publishing our initial Equity Research just two months ago, we review the results reported this Friday, update our spreadsheet, and share our conclusions on this company that has lost more than 50% of its market cap over the last 6 months.