Golar LNG - Full Analysis post Argentina deal

Its destiny is set in stone

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Golar LNG - Coinciding with the 5th anniversary of our first investment, Golar announced this Friday the FID of Argentina’s first FLNG and the contract for a second unit. We've spent the entire weekend running numbers and making calls to bring you the most comprehensive analysis possible (including a downloadable spreadsheet with the DCF model) of the deal—covering assets, the SESA analysis, and Golar LNG's current situation. An in-depth report worthy of all the years we've spent analyzing this company.

Owens-Illinois - In depth Analysis of the Potential Turnaround Story of the World’s Largest Glass Producer

Portfolio Management

Including updates on our 3-stage monitor, commentary on several companies, our macro views, and strategies for managing the portfolio in today’s challenging environment. Also included are the corresponding movements in both our equities and multi-asset portfolios

Good Times Restaurants - Meeting with its CEO (Ryan Zink)

Investor Resources

Data Center Update - Including our first created plugin for Options

Nota: Toda esta publicación está disponible en Español en nuestra web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

Summary

Another green week for the markets, which seem to have already forgotten the scare from early April. The S&P 500 has now closed in the green for 9 consecutive days, marking the longest streak in 20 years. The main earnings week of the season has surprised to the upside, and macro data on the labor market and unemployment have been solid. This has crushed the odds of the Fed cutting rates this upcoming Wednesday.

The one negative note was the drop in GDP (significantly more than expected, largely due to front-loaded imports ahead of the tariffs — something we’ve discussed here in recent weeks with the Atlanta Fed’s forecast). However, the market took it positively since consumption remains relatively healthy, and overall there hasn’t been much market reaction. On the tariff front, no agreements have been reached yet, but the tone from the U.S. administration has notably improved.

However, attention should be drawn to the options market. There, the story diverges significantly from the index rallies, as put-buying volume (especially on the S&P 500) far exceeds call-buying, creating a very pronounced skew. In other words, some asset managers are being forced to buy into the rally but are mainly protecting themselves against a potential drop. Let’s see how the second half of the month plays out with the expirations on the 16th and the container supply cycle in the back half of the month (tariff implementation + shipping time to NY).

Regarding the major companies, earnings have not only been strong, but Microsoft and Meta pointed to continued Capex in artificial intelligence and datacenter growth, which came as a huge relief for the sector amid recent fears of a slowdown and the impact of tariffs. That said, companies with greater exposure to tariffs and consumer spending — especially smaller ones — are consistently noting in meetings and earnings calls that they’re taking a very conservative approach to decision-making and that uncertainty remains extremely high.

Commodities were the week’s biggest losers, as China’s macro data was poor (and commodities move hand in hand with China). Oil is reflecting global slowdown fears (with declines over 25%, clearly signaling recession worries), and Chinese bonds are at multi-decade lows.

This coming week, earnings season begins to slow down, but all eyes will be on the Fed on Wednesday. And honestly, given last week’s data, a rate cut is practically off the table. That’s something the U.S. administration won’t like — and we might see some incendiary statements in response.

Macro highlights

US Employment data

In April, 177,000 new non-farm payroll jobs were added—well above the 138,000 that analysts had expected. While that’s a solid number, it still came in below the initial March figure of 228,000, which was later revised down to 185,000.This marks the third consecutive downward adjustment to job figures. In total, 58,000 jobs were effectively erased after revisions to the data from February and March.

Looking at individual sectors:

Healthcare saw the largest gains with 51,000 new jobs.

Transportation and warehousing added 29,000.

Financial services grew by 14,000.

Social assistance increased by 8,000, though at a slower pace.

Federal government employment declined by 9,000 in April, bringing total losses to 26,000 since the start of the year.

Excluding roles in government, education, and healthcare, private sector hiring was steady in both March and April, with 96,000 and 97,000 jobs added, respectively.

The unemployment rate held steady at 4.2% in April, effectively unchanged from March (4.187% vs. 4.152%). It’s remained between 4.0% and 4.2% since May 2024.

Additionally, the number of full-time workers rose by 305,000, while part-time employment increased by 56,000.

US GDP

The U.S. GDP for Q1 2025 came in at -0.3%, marking a sharp reversal from the +2.4% growth seen in Q4 and falling short of the expected -0.2%.

Breaking down the components of first-quarter GDP:

Personal consumption contributed 1.21%, down significantly from 2.70% the previous quarter. Still, in annualized terms, that equates to a 1.8% growth rate, beating the forecast of 1.2%.

Fixed investment bounced back, contributing 1.34% compared to -0.2% in Q4. This is the strongest figure since Q2 2023, in part because the BEA has started properly accounting for investment in data centers, which boosted the numbers.

Private inventory changes added 2.25% to growth, a dramatic swing from the previous quarter’s -0.84%. This spike was expected and largely driven by stockpiling ahead of upcoming tariffs. However, this is likely to unwind in the coming quarters as inventories are drawn down.

Government spending subtracted 0.25% from GDP, marking the first negative contribution from the public sector since 2022. While the decline wasn’t large, it stood out in the context of recent quarters where government outlays had been a key growth driver.

The biggest drag came from net trade (exports minus imports), which shaved off a substantial 4.83% from GDP. That’s a massive reversal from the +0.26% contribution in Q4 and now stands as the largest negative trade impact ever recorded. The reason? A surge in imports ahead of new tariffs which distorts the GDP calculation even though it doesn’t reflect weaker real economic activity.

US PCE

March PCE inflation came in soft, aligning with expectations.

Core PCE rose just 0.03%, keeping the annual rate at 2.6% after February was revised up.

Headline PCE fell 0.04%, lowering the 12-month rate to 2.3%.

Details:

Core goods dropped -0.27%, reversing prior gains.

Housing jumped +0.39%, the highest since October.

Core services ex-housing slowed sharply to +0.04%.

Despite the soft March reading, short-term inflation remains sticky, with the 3- and 6-month annualized core PCE rates at 3.5% and 3.0%, both above the 12-month trend.

Interesting Data about markets this week & YTD

It was a good week mainly for Asian currencies versus the US dollar, and a generally positive one for equity markets around the world — with the exception of Russia, Argentina, and Turkey.

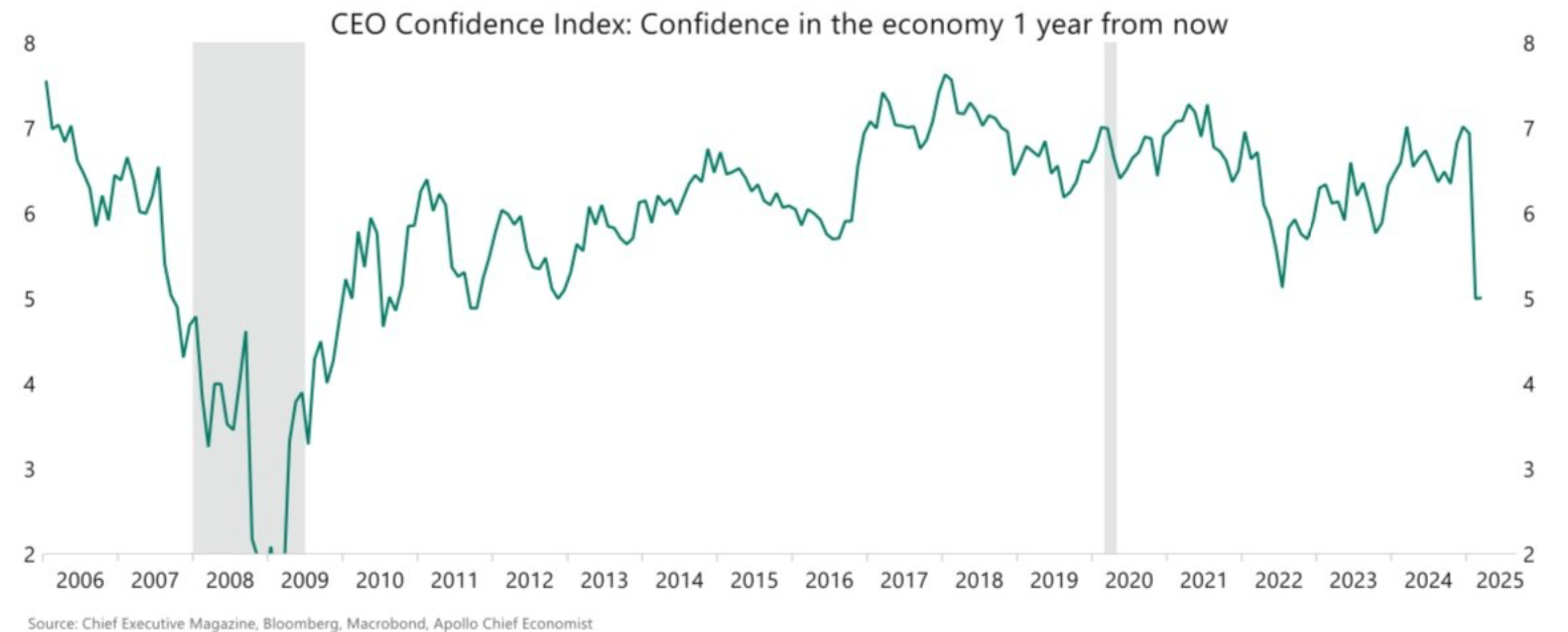

After analysts had been cutting 1Q25 earnings estimates for 17 consecutive weeks (and were clearly way off), the focus of the downgrades has now shifted to 2Q25. And in this case, we do share the view — after speaking with several small and mid-cap companies, decision-making is currently at a complete standstill, closely tied to the levels of uncertainty shown in the next chart.

Earning Season 2Q25

Now that most of the major S&P 500 companies have reported (with NVIDIA being the main one still pending), it's time for the companies in our coverage universe to start reporting. This week: Campari, Good Times Restaurants, New Fortress Energy, Fortress Infrastructure, Cheniere, Newlat, GOGO… and next week, the superyachts.

Updated Investment Thesis - Golar LNG

Golar LNG, the company for which MORAM Capital is probably best known, the one we’ve spent the most time analysing and of which we’ve been investors for 5 years now (this week), has signed this week an agreement of vital importance, committing two of its three assets for 20 years in Argentina.

Golar has completed its transformation over the past few years, evolving from a shipping company (operating LNG transport vessels) into a pure liquefied natural gas infrastructure company. This shift was driven by its flagship value proposition, the FLNG (Floating LNG)—a specialized type of vessel that functions as an offshore LNG terminal. Golar is a pioneer in this solution and the world’s leading company in this field. These assets are characterized by long-term contracts, providing fixed and predictable free cash flows, with potential upside from natural gas prices (such as those announced this past Friday).

Golar has two operational FLNG units (Golar Gimi 2.7 MTPA, being commissioned to begin this month a 20-year contract with BP in Senegal/Mauritania—it recently announced the receipt of a $220MM indemnity for the delay in the start; Golar Hilli 2.45 MTPA, under contract in Cameroon with Perenco until July 2026, after which it will go to Argentina), another under construction (Golar Fuji, 3.5 MTPA for Argentina) and a fourth planned for which they are negotiating contracts in several countries in Africa, Southeast Asia, and Latin America. It also has Macaw Energies. The FLNG negotiations usually take quite some time (Golar’s last contract signing was in 2018), which is why this week’s step is so important (we’ll comment later on the market reaction / sell the news).

In Argentina, both units will work together, Hilli starting around 3Q27 and Fuji (Mark II) in 4Q28, in what will be the first phase of the Argentina LNG project, led by YPF in consortium with Pan American Energy, Harbour Energy, Pampa Energía, and Golar itself, which holds a 10% stake in the project (we analyse the business case of Southern Energy in detail further below). The second and third phase of the project will also be carried out using FLNG but with owned vessels (Shell and ENI) and not Golar’s, due to the tremendous economics of the deal for the company providing the liquefaction vessels (in Phase I, Golar).

The contract is complex, and we’ve spent the whole weekend making calls here and there to confirm (as much as possible) some of the things that are said and not said, but as of today, we believe that the DCF model we’re sharing (downloadable) to value the company, the level of detail analyzing the assets (FLNGs), and our share in the company and independent opinion on the situation is among the most complete you can find on the internet.

Today, we are sharing:

Explanation of the details of the new contracts in Argentina and assumptions necessary to understand all dependencies

Economics of Southern Energy

Economics of the new Hilli and Fuji (Mark II) contracts

Valuation (DCF model & metrics) under different scenarios (downloadable spreadsheet)

Our perspective on the current situation

Incredible level of detail, for the company we know best.