Italmobiliare Investing Holding - Analysis

Access to fantastic businesses at rock-bottom prices

Hi there!

This week

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Earnings season…

Italmobiliare Investing Holding - Analysis of a European Family Holding that focuses on acquiring small to mid-sized non-listed Italian companies with an emphasis on high quality, aiming for a medium-term investment horizon. It leverages its knowledge, experience, and corporate governance to scale these companies and make them larger and more efficient, preparing them for potential sale or IPO. It currently trades at a significant discount versus NAV and owns highly interesting companies with strong potential for the coming years. Full independent valuation & our thoughts

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Data Center

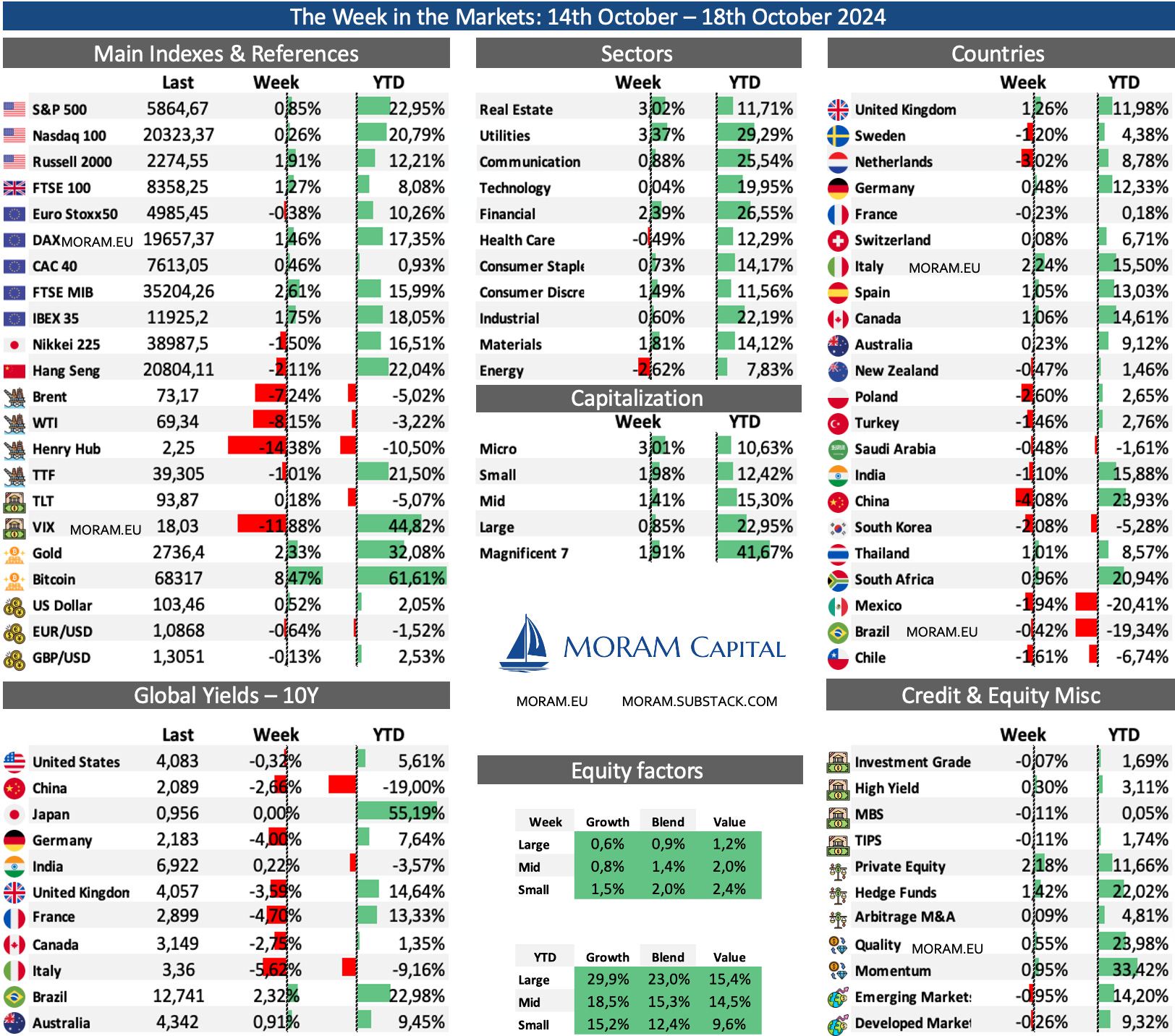

The Week in the Markets

New highs for the S&P 500 came during a week marked by the so-called "Trump Trade," as markets began pricing in the possibility that he could be the next president of the United States. Small caps, Bitcoin, and the dollar were among the week's biggest winners.

By Thursday’s market close, the gap between the Russell 2000 and Nasdaq had widened by over 4%. However, strong results from Netflix and Taiwan Semiconductors gave the Nasdaq a boost on Friday, closing the week in positive territory. Earlier in the week, ASML had seen its largest drop since 2008, falling 15% after its earnings report, erasing all of its 2024 gains.

In terms of sectors, Real Estate and Utilities were the best performers, benefiting from falling interest rates, while Energy closed in the red due to a sharp drop in oil prices driven by lower expectations of Israeli attacks on Iran’s oil and gas infrastructure.

In Europe, most major indices closed positively, as the ECB continued its rate cuts. In China, despite a slight rise in the Shanghai Index (local currency), both the Hang Seng and MSCI (in U.S. Dollars) saw sharp declines.

Gold hit all-time highs, up 32% so far in 2024, while the VIX dropped sharply but remained at 18, amid developments in the Middle East and macroeconomic data.

10-year bonds ended the week in negative territory, despite a brief surge on Wednesday following positive retail sales data. This was due to news that the number of building permits and housing starts both decreased in September.

Highlights of the week

Europe

The ECB cut the three main interest rates by 25 basis points as expected:

The deposit facility rate was reduced by 25 basis points to 3.25% from 3.50%, as anticipated.

The main refinancing rate was lowered by 25 basis points to 3.40%.

The marginal lending facility rate was cut by 25 basis points to 3.65%.

The cut was motivated by weaker-than-expected economic activity indicators with the ECB reiterating it will maintain restrictive policies as long as necessary

The ECB acknowledged that "the disinflationary process is on track," and analysts expect further rate cuts. Europe’s manufacturing and macroeconomic indicators are lagging behind the U.S., and the ECB faces two choices: cut rates more aggressively than the U.S., potentially weakening the euro, or match the U.S.'s pace, risking further damage to the economy. For now, it seems to be leaning towards the first option.

Annual inflation in Europe fell to 1.7% (down from the 2.2% reported last month), which suggests to us (as well as to the market) that rates are likely to be lowered again in December.

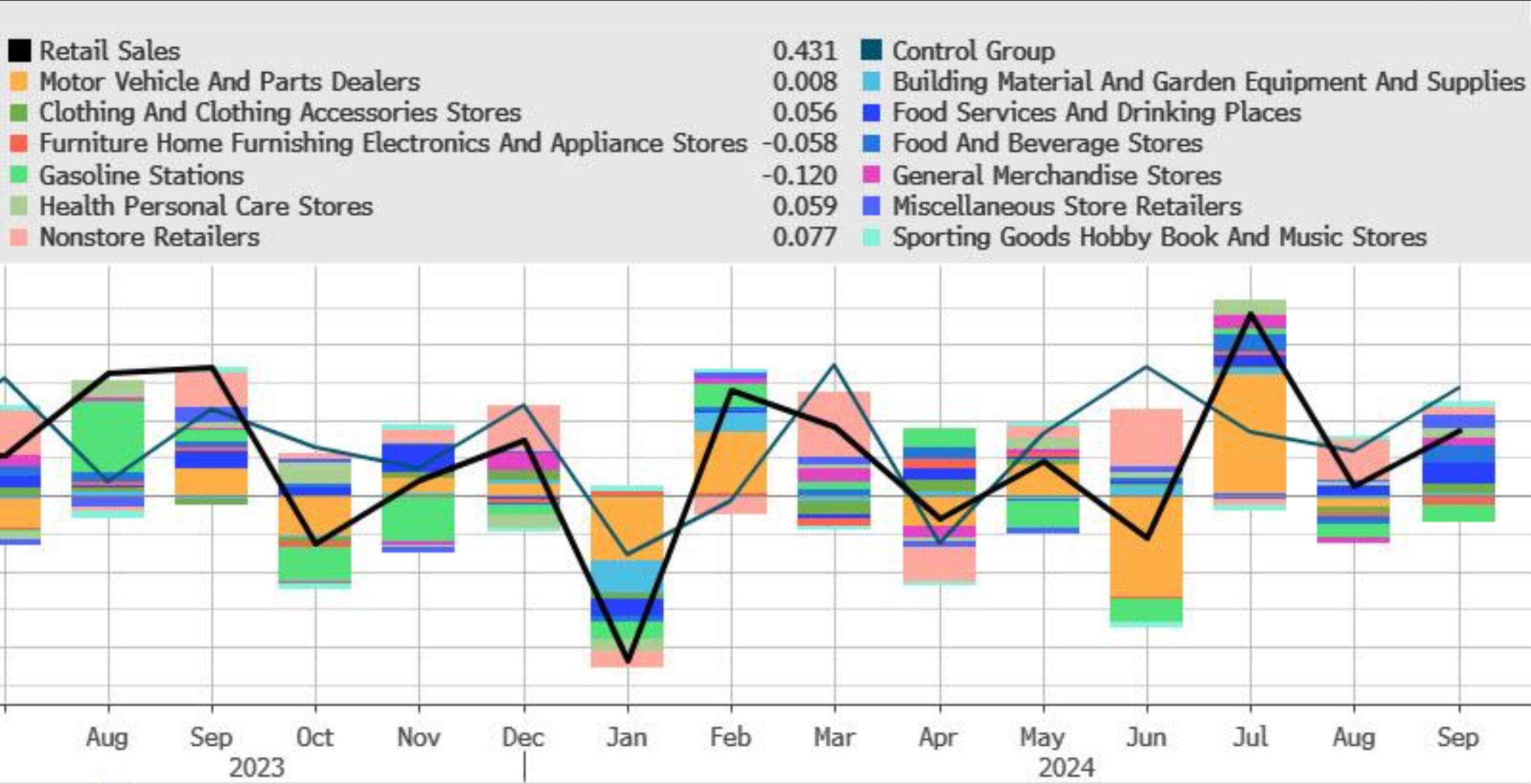

US Retail Sales

U.S. retail sales grew 0.4% MoM in September 2024, exceeding both August's 0.1% rise and expectations of 0.3%. Despite this, annual growth slowed to +1.7%, the weakest since January. The control group saw sales rise for the fifth straight month (+0.7%), making a significant GDP slowdown unlikely. Notably, unadjusted retail sales dropped 7.5%, the largest positive seasonal adjustment on record for September.

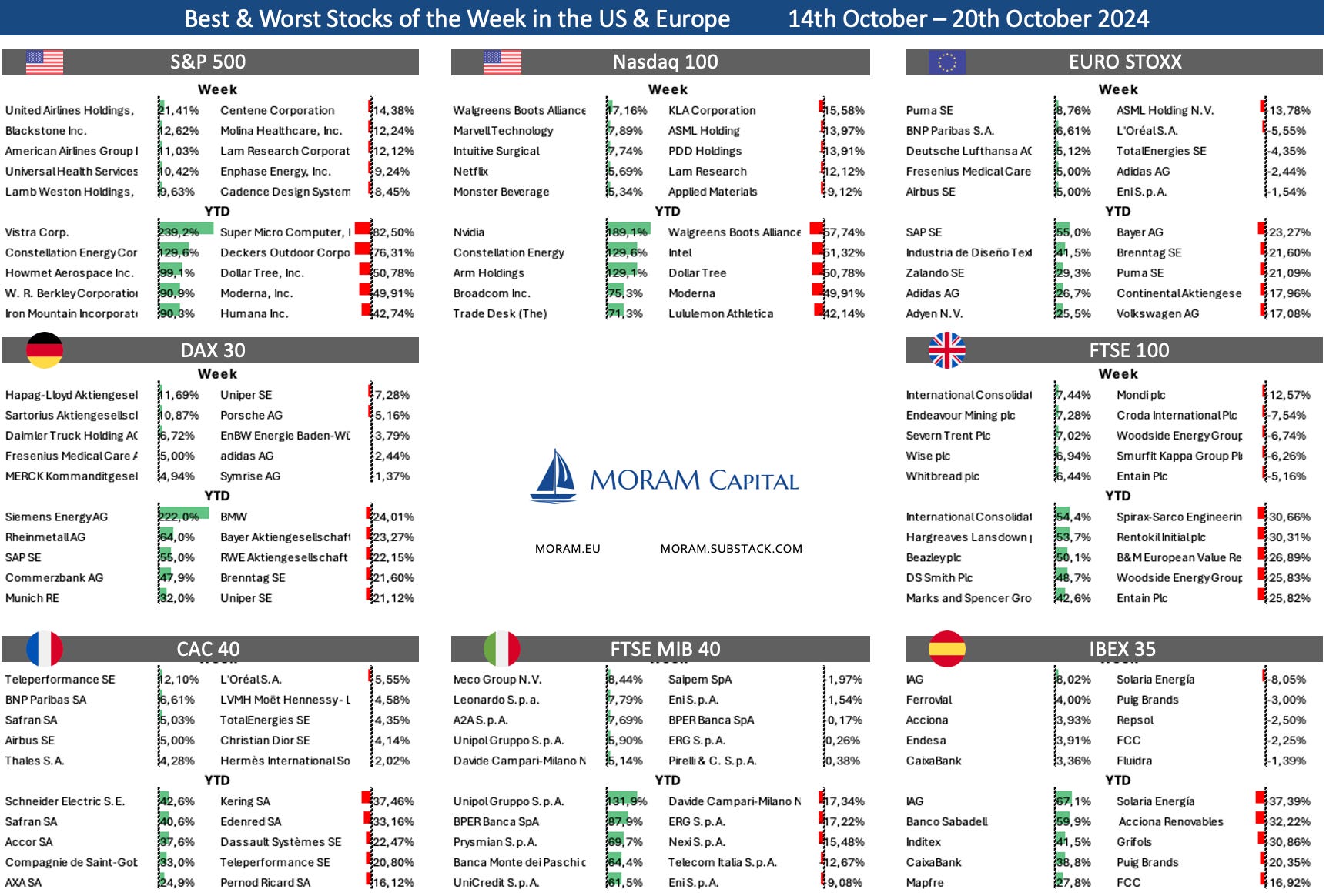

Some interesting Data about markets this week & YTD

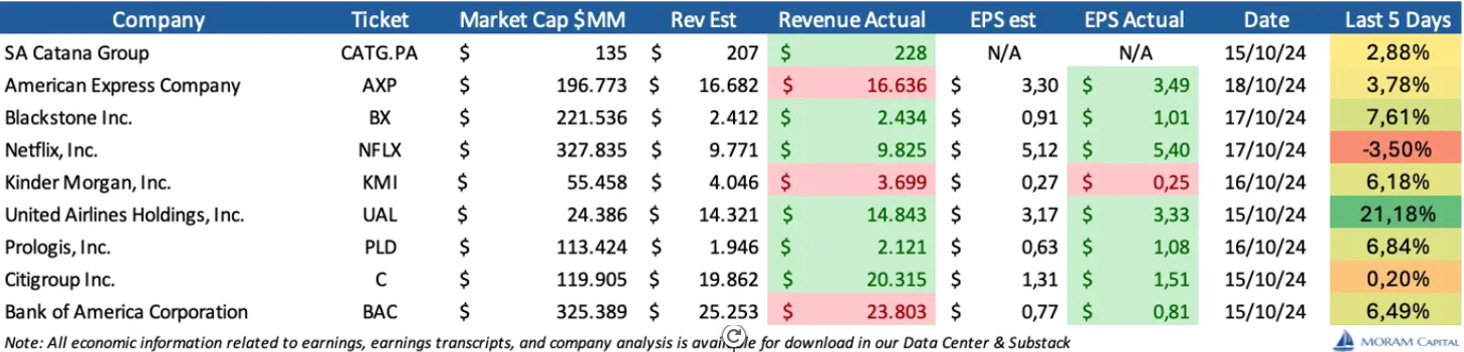

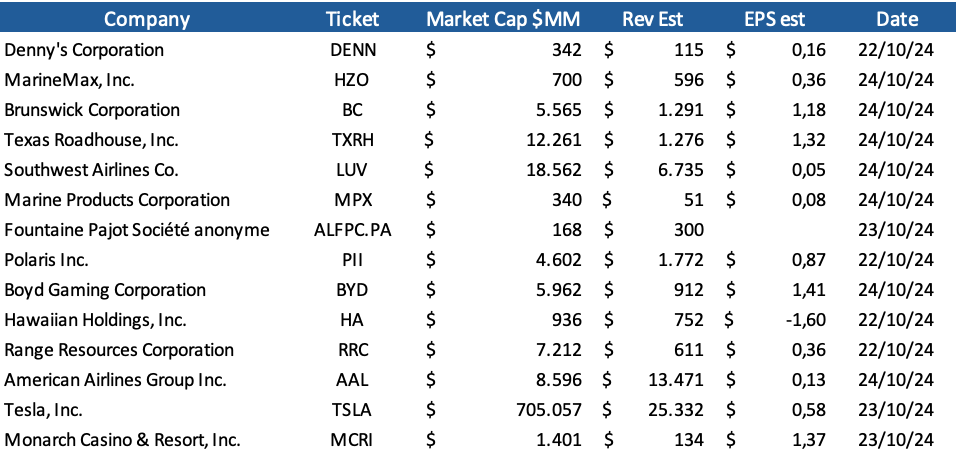

Earning Season

For this upcoming week, many airlines, the first reports from restaurants, and also other industries of our interest such as boat manufacturers and dealers. Likewise, the Mag 7 begin, with Tesla on Wednesday

Italmobiliare Investment Holding - Analysis

Last week, we wrote an introduction to the European Family Holdings industry, in which, besides discussing Exor, probably the best-known name, we also mentioned other relevant players in the industry.

Most of these players are companies with several billion in market capitalization, but among them, the performance of two small Italian players stood out: Tamburi Investment Partners—about which we wrote extensively, explaining the company, independently valuing its holdings, and sharing the valuation model and our conclusions—and Italmobiliare, which we will cover in the same way today.

There are significant differences between Italmobiliare and Tamburi that we explain throughout the analysis, but some key ones are that Italmobiliare:

Invests primarily in unlisted companies (more than 60% of Tamburi’s investments are in listed companies),

Has a much larger discount to NAV,

Has a much shorter track record (since 2016, as we explained in the introduction).

Governance model, Capital Allocation, Investment sectors, …

Introduction to Italmobiliare

Italmobiliare is an Italian holding company that, despite having nearly 80 years of history, only truly began its journey as the holding company we know today in 2016. In fact, its beginnings are somewhat peculiar, as it was founded in 1946 by the cement company Italcementi, as a vehicle to hold investments outside of the construction materials sector. Its early years were focused on investments in the automotive sector and local credit companies. In 1979, it acquired a majority stake in Italcementi and became the holding for the entire group (with a strong dependence on Italcementi). In 1984, it made its IPO, and in the following years, it continued investing in credit companies, publishing media, and the automotive sector.

It was in 2016 when Italmobiliare sold the remaining 45% stake in Italcementi to HeidelbergCement (announced in July 2015) and transformed into the company we know today. Italmobiliare received €878 MM in cash and 10.5 MM newly issued shares of HeidelbergCement (Italmobiliare became the second-largest shareholder of HeidelbergCement with a 5.3% stake). Additionally, Italmobiliare agreed to purchase Italgen S.p.A., Bravosolution S.p.A., and certain non-core real estate assets from Italcementi for €237 MM, which remain part of Italmobiliare today. This amount of cash (and shares of HeidelbergCement, which they have gradually reduced) has allowed Italmobiliare, in the following years, to build the portfolio they have today.

We believe this introduction is important to start comparing Italmobiliare with its peers from 2016/2017 onwards, rather than over a longer track record, as previously, it traded largely with the cyclicality of a cement company.

Investment Strategy

Italmobiliare Investment Holdings focuses on acquiring small to mid-sized non-listed Italian companies with an emphasis on high quality, aiming for a medium-term investment horizon. The goal is to leverage its knowledge, experience, and corporate governance to scale these companies and make them larger and more efficient, preparing them for potential sale or IPO.

The current portfolio of non-listed assets showcases a diverse range of sectors, primarily focused on Italy and Europe, which accounts for approximately 90% of sales. However, one of the characteristics of the companies they target is their potential for internationalization, so this percentage should continue to decrease in the coming years.

Italmobiliare’s portfolio can be divided into five different segments, which are detailed as follows:

Portfolio Companies: This includes 11 affiliated companies (most of which have a majority stake) to leverage Italmobiliare’s expertise in managing business operations and driving growth. The companies contributing the most to NAV are Caffè Borbone, Santa Maria Novella, Tecnica, Italgen, and Cassa della Salute.

Private Equity Funds: These funds aim to capitalize on opportunities in geographical areas or business sectors where Italmobiliare is not directly involved while fostering potential business development in diversified sectors. 40% of the value of these investments is managed through a management company in which they own 100% (one of the 11 portfolio companies).

Other Investments: This segment consists of minority investments across various sectors (both listed and unlisted companies) that offer promising growth prospects or stable investment returns For Example, they have an stake in Argea (a competitor of Italian Wine Brands)

Real Estate: This aspect is a legacy from their transaction with HeidelbergCement, which involved acquiring several assets in Italy, primarily in Rome.

Financial Investments, trading & liquidity

Unlike Tamburi, which we reviewed last week, Italmobiliare primarily focuses on investments in private companies, mainly through direct investment in significant stakes that enable them to have an important role managing the companies leveraging its experience, financial resources and network. Despite being private companies, Italmobiliare exercises a lot of transparency by publishing the financial statements of the companies and providing detailed information about them

Another notable point is that the debt is mainly held within the companies themselves, which makes it relatively straightforward to understand their structure and financial situation, which we will explore in more detail later.

Holdings

Caffè Borbone (2018)

Caffè Borbone is the main holding of Italmobiliare, a coffee manufacturer founded in Naples in 1997. In 2018, Italmobiliare acquired a 60% stake for €143 million (implying an 8.6x EV/EBITDA), with the remainder held by its founder.

Caffè Borbone specializes in coffee capsules (52% of its revenues) compatible with major coffee machine brands like Lavazza, Nespresso, and Nestlé Dolce Gusto. Despite its relative youth, it has become one of the leaders in Italy (alongside Nespresso and Lavazza) due to its quality-price proposition (Borbone capsules cost around €0.20 compared to €0.40-€0.50 for the others).

The single-serve coffee market is the fastest-growing segment within the coffee industry, although it still only represents about 12%. This essence of making quality Neapolitan coffee accessible at reasonable prices has allowed for tremendous growth in recent years, with a revenue CAGR of 19.5% over the past seven years and EBITDA margins exceeding 25%.

With 92% of its sales in Italy, one of the company's major growth pillars is international expansion, particularly in the United States—a country very receptive to all things related to Italian food. Although still in its early stages, this strategy has begun to yield results; last year, sales in the U.S. grew by 60%, and this year a strong increase is expected (on track to represent 5% of the group’s sales). Another significant growth area, although it has improved notably in the last three years, is northern Italy, where brand awareness is much lower, as prior to Italmobiliare's acquisition, sales were almost exclusively concentrated in the south.

Caffè Borbone employs a multi-channel B2B2C approach, aiming to cover all of Italy. This strategy helps target various customer types and market segments, contributing to its strong domestic growth. The company sells through a diversified network, including specialized shops, Office Coffee Service (OCS), and large-scale distribution outlets, which perform best and are growing the fastest.

In recent years, they have focused on distributing their products via Amazon, which is growing rapidly (+32% YoY) and already accounts for nearly 15% of the company’s sales.

Alongside its distribution strategy, Caffè Borbone is making significant efforts in marketing to increase brand recognition beyond southern Italy, as well as developing eco-friendly and sustainable products (a growing concern among customers in the capsule business). They consistently invest in research and development to launch new products (like Crema Fredda Caffè and MokaCiao) and adapt them to local needs, such as a fully compostable K-cup capsule for the U.S. market. Similarly, they also sell coffee machines and tea-related products.

Economics

Caffè Borbone has experienced rapid growth in recent years due to its quality/price ratio compared to its competitors and the significant growth opportunity provided by a company like Italmobiliare. In the coming years, this growth is expected to focus primarily on international markets, where they have made considerable progress in the U.S. over recent years.

The business model is—barring some differences—similar to that of Italian Wine Brands, meaning they buy raw materials (coffee) directly, manufacture in Naples at a cost of just 8 cents per capsule, and distribute them at around 20 cents (significantly lower than Nespresso/Lavazza but with substantial margins).

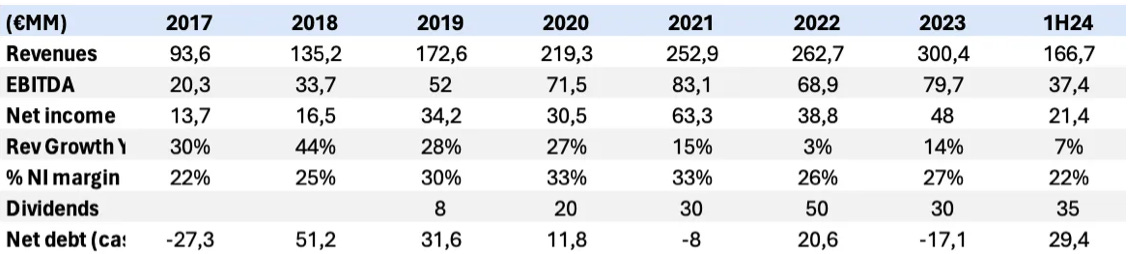

Forecasts for 2024 indicate significant (double-digit) revenue growth, although margins will be impacted by the rising coffee prices, which have only been partially passed on to consumers (leading to an expected EBITDA lower than last year, projected between €72-75MM). Additionally, in the first half of 2024, cash generation was -€11.3MM, mainly due to the absorption of working capital amounting to €25.0 million, driven by increased raw coffee inventory. The cash/net debt already accounts for the dividend payment.

Regarding the valuation presented alongside other companies, we have based it on comparative metrics with peers like JDE Peets or Massimo Zanetti (Segafredo).

Santa Maria Novella (2020)

Officina Profumo-Farmaceutica di Santa Maria Novella is the second most important holding of Italmobiliare. It is a company that produces and distributes luxury fragrances and cosmetic products under its own brand. Founded in 1221, its flagship store—also a museum attracting more than 500,000 visitors annually—is located next to the iconic cathedral of Florence, sharing its name.

Italmobiliare made its initial investment in 2020, focusing on driving international growth and increasing marketing activities, which were previously almost non-existent.

The company sells its products through three channels:

Wholesale (selling products in bulk to retailers or other businesses): This accounts for 40% of its business but has been losing importance compared to previous years. Currently, they are focusing on global partnership agreements to open new stores, including a recent one in the UAE. They already have more than 200 wholesale stores in Europe, the USA, and Asia.

DOS (Directly Operated Stores): This is the main segment, contributing 48% of current sales through its more than 100 stores, and the company is focusing heavily on growing it (along with distribution partnerships mentioned before). Recently, they bought back the distributor in Venice and the distribution business in Japan with 16 points of sale (effective in 2024) and plan to open more DOS locations in Paris, London, and the USA soon.