Significant opportunities in the European Superyachts industry

Sanlorenzo, The Italian Sea Group, Ferretti

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

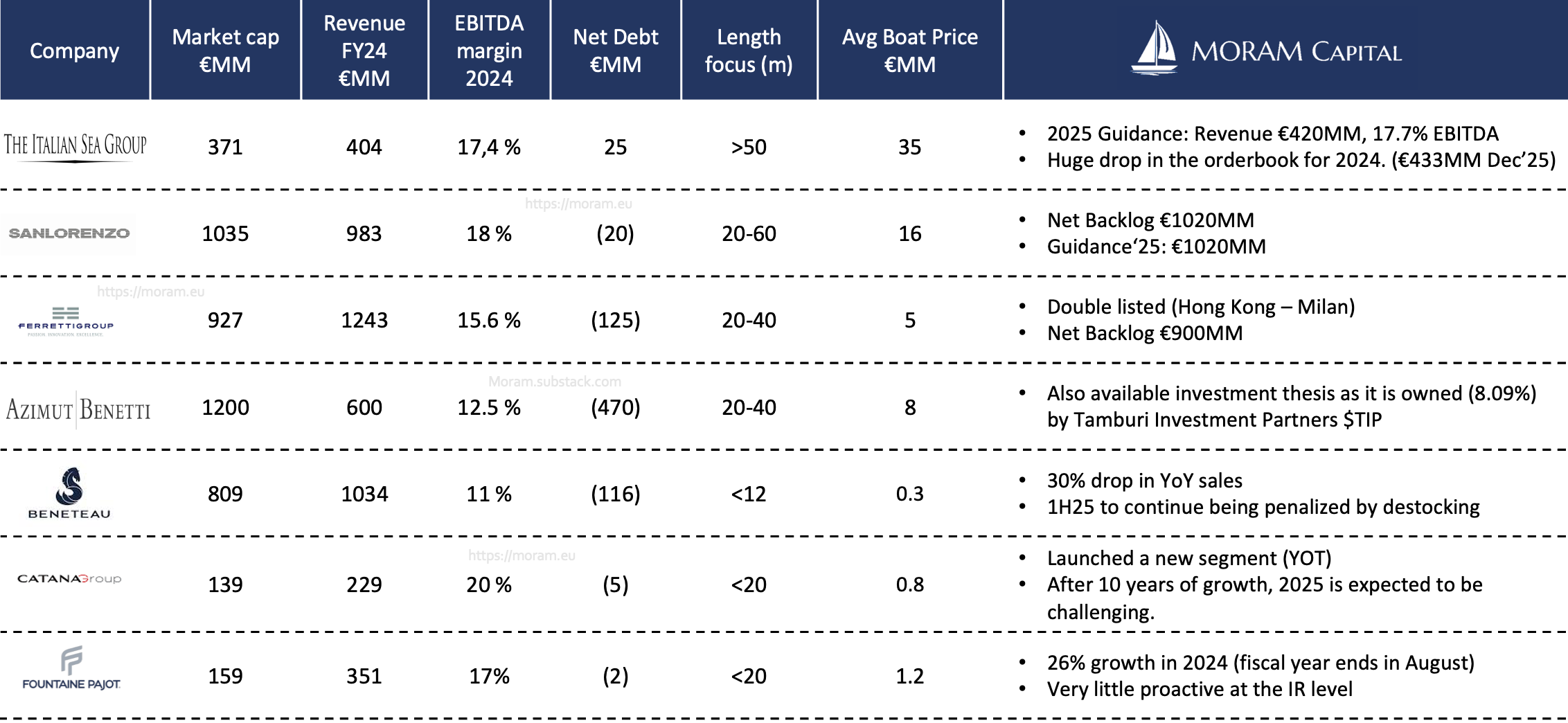

European Superyacht Industry - As every quarter, the most comprehensive analysis of an industry we have been covering for four years. Updated valuations, FY24 earnings comments, comparative analysis of each company's situation and our thoughts about positioning in the industry. Individual analysis for each company available.

The Italian Sea Group - Detailed analysis following Friday’s results and the subsequent drop due to doubts about meeting the provided guidance, given the weak order intake over the past six months. DCF model, backlog analysis, geographies, conference call comments... and our perspective on the company.

IDT - family-owned US conglomerate of companies that has produced an amazing return since it was founded 1990. If one had held IDT and its spinoffs during the decade from 2010-2020, one would have a CAGR of +50%.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (also include lot of details about the companies reporting these weeks).

Investor Resources

Data Center Update

Financial model Updates

Nota: Toda esta publicación está disponible en Español en nuestra web

Disclaimer: This publication is for educational purposes only. Nothing presented here constitutes investment advice. Before making any investment decisions, consult your advisor.

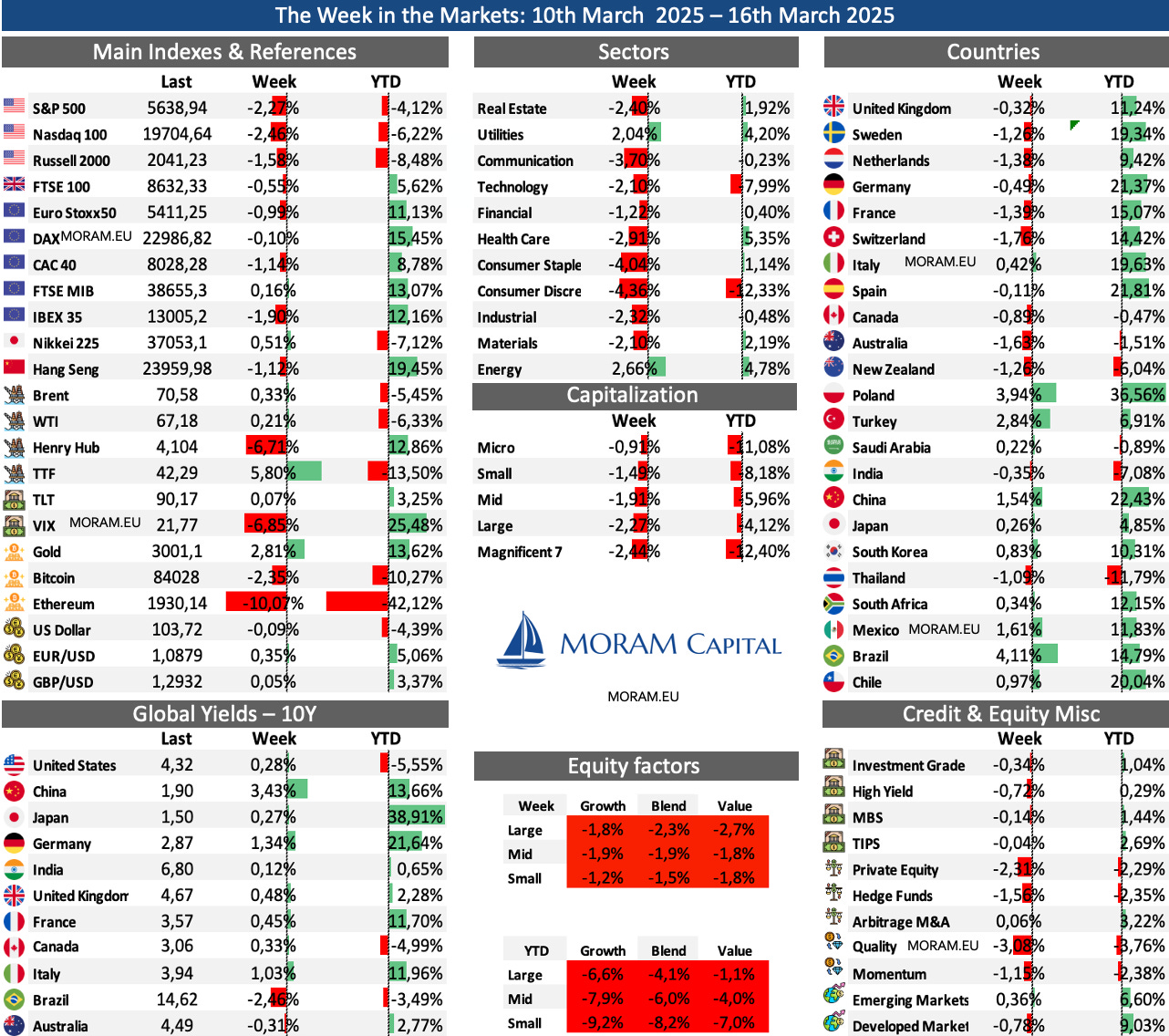

The Week in the Markets

Summary

Fourth consecutive week of losses for the major U.S. indices, once again with the Mag7 (30% weight in the S&P 500 and >35% in the Nasdaq 100) underperforming the S&P 500 Equal Weight. Markets struggled this week amid ongoing trade uncertainty following new tariffs from the Trump administration. Additionally, recession fears continued to grow, especially after Trump referred to a “period of transition” for the U.S. economy. However, on the macro level, the Core CPI provided significant relief with its lowest YoY increase since April 2021 (+3.1%), as did the PPI released on Thursday.

The Nasdaq was the worst-performing of the major indices this week, partly dragged down by Apple, which fell 10.7% (and Tesla and Alphabet, which dropped nearly 5%). The tech benchmark index is down -6.22% YTD, having already fallen more than 10% from its yearly highs four weeks ago.

Beyond the U.S., this week only the Japanese Nikkei is performing well, as neither China nor Europe (with YTD returns of 19% and 15%, respectively) could continue their positive streak.

In fact, our equity factors map (representing only U.S. companies) is now completely (and for the first time this year) red. Last week, large-cap value companies were still holding up, but with this week’s 2.7% drop, they have entered negative territory.

In commodities, the trend has reversed compared to earlier this year, with Henry Hub rising and oil and European gas prices falling. However, despite oil having a negative YTD of around 6%, energy stocks are the second-best sector YTD, closing the week as the only sector in the green, alongside utilities.

Gold reached historic highs, crossing the psychological barrier of $3,000/oz for the first time. A 13% YTD return for gold is an absolute anomaly. Meanwhile, the VIX gave some respite this week despite the red across the markets, and the 10-year Treasury yields closed above 4.3%. Emerging markets, primarily driven by Latin America, Turkey, and Egypt (details in the next section), have outperformed developed markets by a significant margin.

Overall, volatility remains the dominant trend for yet another week, with major global stock markets at key support levels, earnings season coming to an end, and the Fed meeting this Wednesday, likely to keep monetary policy unchanged.

Macro highlights

CPI

Inflation rose less than expected in February. 2.8% YoY (2.9% expected) and 0.216% MoM, lower than last month’s +0.467% and below the expected +0.28%.

Housing contributed +0.29%, accounting for nearly half of the monthly CPI increase, though WisdomTree estimates real-time shelter inflation at 1.5%, much lower than the BLS's official 4.2%. This was offset by a 4.0% drop in airfares and a 1.0% decline in gasoline.

SuperCore CPI (services ex-housing) rose just 0.215%, well below last month’s +0.757%, bringing the annual rate to 3.91%, the lowest since October 2023.

Overall, the disinflation trend in services continues after last month’s spike, while goods have stopped dragging inflation down and are now contributing slightly.

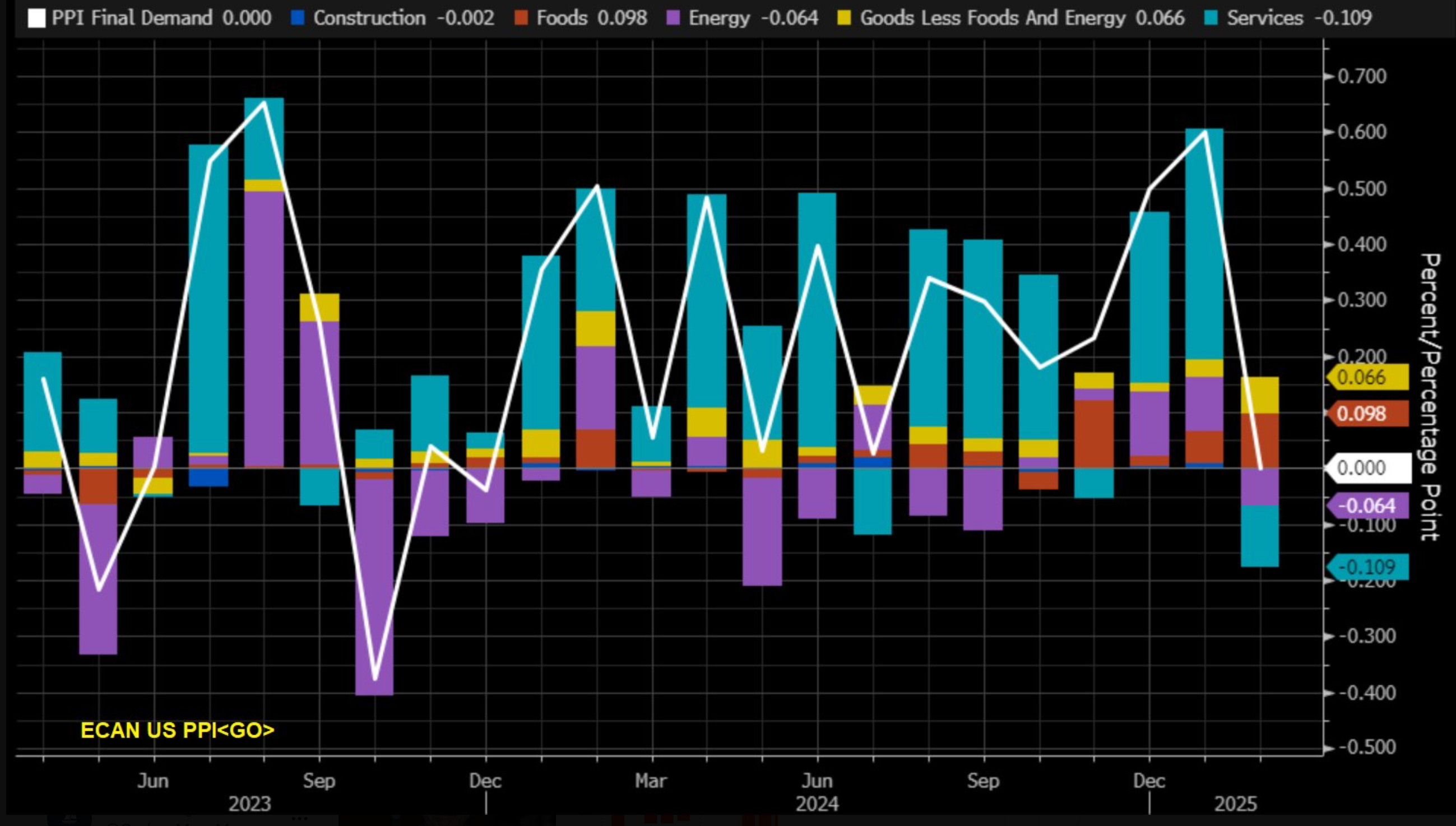

PPI

The PPI also provided some relief (YoY 3.2%, below expectations of 3.3% and Core PPI 3.4%, below expectations of 3.6%. MoM 0%)—inline with the CPI—although several of its key components (which also impact the PCE—the Fed’s preferred metric for interest rate decisions) remain elevated, leading the market to believe that the Fed will keep rates unchanged in its meeting next week.

Consumer confidence (University of Michigan)

Consumer sentiment keeps deteriorating—Michigan's index fell 11% in March to 57.9, marking its third consecutive drop and a 22% decline since December 2024. The report highlights worsening expectations across personal finances, jobs, inflation, and markets, driven by policy and economic uncertainty.

Notably, year-ahead inflation expectations jumped to 4.9%, the highest since November 2022 and the third straight monthly increase of 0.5% or more.

Europe

After the ECB's sixth rate cut since June, several policymakers cast doubt on another cut in April. Lagarde cited high uncertainty in meeting the 2% inflation target, while Schnabel warned inflation might stay above target. Kazaks suggested caution due to geopolitical risks and defense spending. In contrast, Centeno called for even lower rates to support the economy and prevent inflation from falling too low.

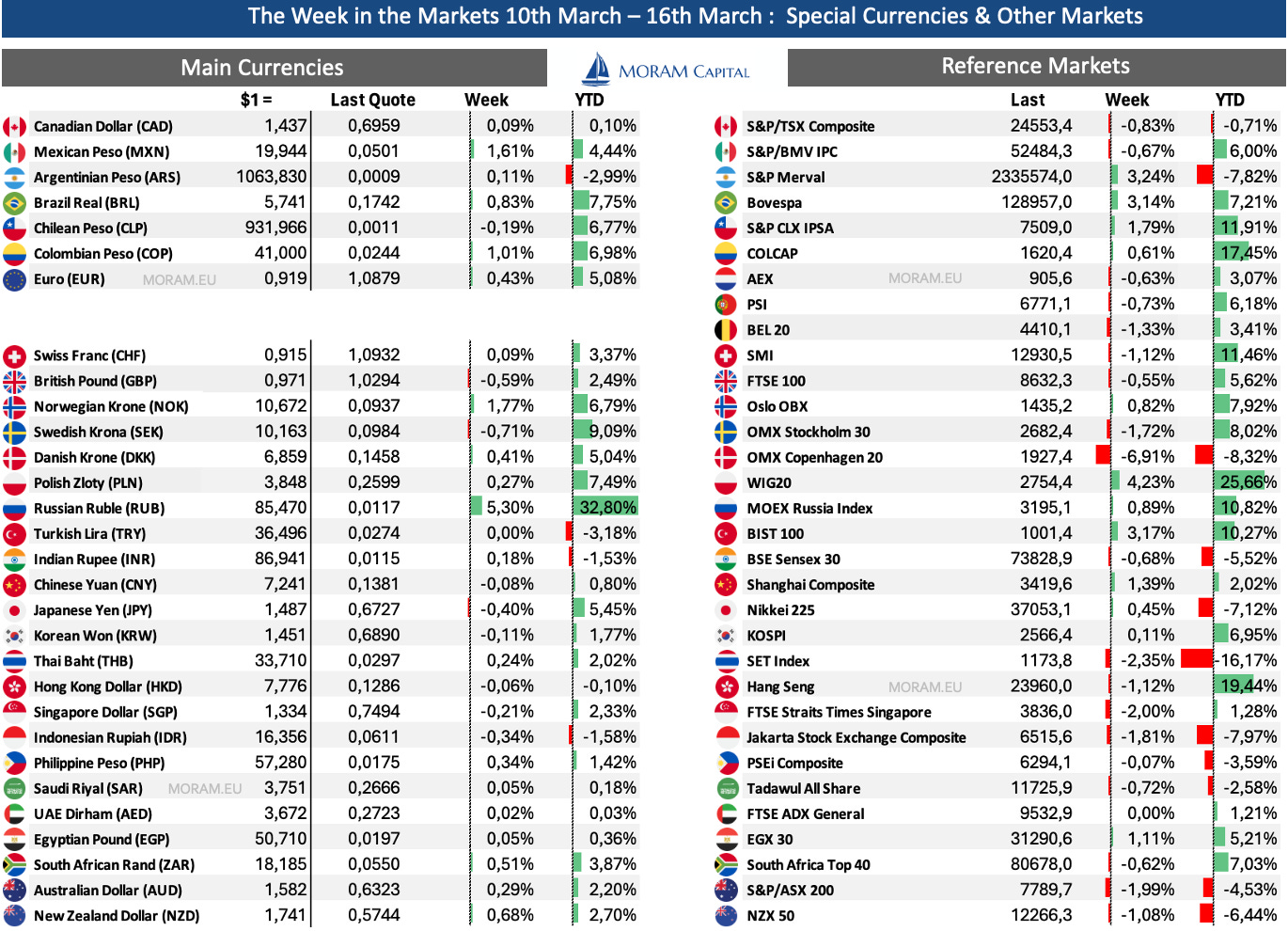

Interesting Data about markets this week & YTD

The Polish stock market continues to stand out for another week as the best in the world in 2025, already up more than 25%. It was a very good week overall for Latin America, with Brazil and Argentina rising more than 3%, as well as for Turkey and Egypt. On the negative side, it is worth noting the tremendous fall of the Danish stock market (due to Novo Nordisk) after reporting poor results from the clinical trials of its weight loss drug, CagriSema.

The sharp declines in recent weeks have caused the P/E multiple of the S&P (calculated from the companies that compose it) to drop by more than two points.

Earning Season 1Q25

The S&P 500 earnings season is already coming to an end, although these are the busiest weeks for small and medium companies—the sector in which we specialize at MORAM Capital.

This week, several companies from our coverage universe have reported, and we comment on them here through the Portfolio Management, Special section that we publish—but do not send by email—via chat during the week: Italian Sea Group, SeSa, Arcos Dorados, Gogo,…

Next week, we mainly have Newlat and Epsilon Energy. Here are the main ones from the American market:

Superyachts Earnings Season

The luxury yacht industry is one of the sectors we have dedicated the most time to over the past four years, and it is also one where we are achieving the best results. You have access to a detailed explanation of how the industry operates, the differences between the main types of players, and individual analyses of European yacht and superyacht companies, along with their corresponding valuation models.

As we have been pointing out for over a year now, within the industry, we are seeing very different dynamics between yachts under 24 meters in length and those over 50 meters. In recent months, the 24-meter threshold has even increased to 30 and, in some cases, 35 meters.

It is important to highlight that Beneteau is included here because it is a French company, but in reality, it competes with and follows the dynamics of U.S. boat manufacturers (Brunswick, Malibu, Mastercraft, Marine Products…). Its sales decline has been significantly steeper than its two other French peers because its target audience is less affluent and much more dependent on financing and interest rates.

Similarly, it is worth noting that Catana and Fountaine Pajot’s fiscal year ends in August, and their boat manufacturing process takes at least six months. This means that their FY24 numbers (shown in the table) are still strong, but the decline is ongoing this FY25—especially considering that, as of March, they have yet to provide formal guidance for the year (with first-quarter sales already down 20%).

Especially interesting in the current situation is Italian Superyacht industry, as both Sanlorenzo and The Italian Sea Group have suffered significant declines this week. The former due to the release of its 2025 guidance, and the latter following its earnings report which we will review in detail.

Today, we analyse their situation in detail (backlog, order intake, sales by region, investments, potential M&A, etc.), as there seems to be a clear buying opportunity in both companies. To this, we add the analysis of Ferretti, the third key player, which has navigated the start of the year much more successfully.

Updated downloadable financial models (DCF) as of today and detailed investment theses on the companies are at your disposal.

Honestly, we believe no other website on the internet offers as much information about the industry and its companies as you’ll find in this website