Updated Equity Research: Sanlorenzo, Kosmos Energy & Excelerate Energy

MORAM Capital

Hi there

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Kosmos Energy - Highly leveraged Oil & Gas producer has just reported its 1Q26 results. We analyse whether the rise in the share price already reflects all of the improving operations, higher oil prices, and lower capex intensity, whether there is still upside left, or whether the investment case is starting to become quite risky.

Sanlorenzo - One of the leading players in the global luxury yacht industry, with strong brand positioning and backlog visibility, in a market now facing softer industry demand after several years of exceptional conditions.

Excelerate Energy - The world’s largest dedicated FSRU operator, positioned around long-duration LNG infrastructure contracts and the growing global need for regasification capacity.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update

Financial model Updates

Nota: Tenéis todos los análisis disponible en español en nuestra pagina web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

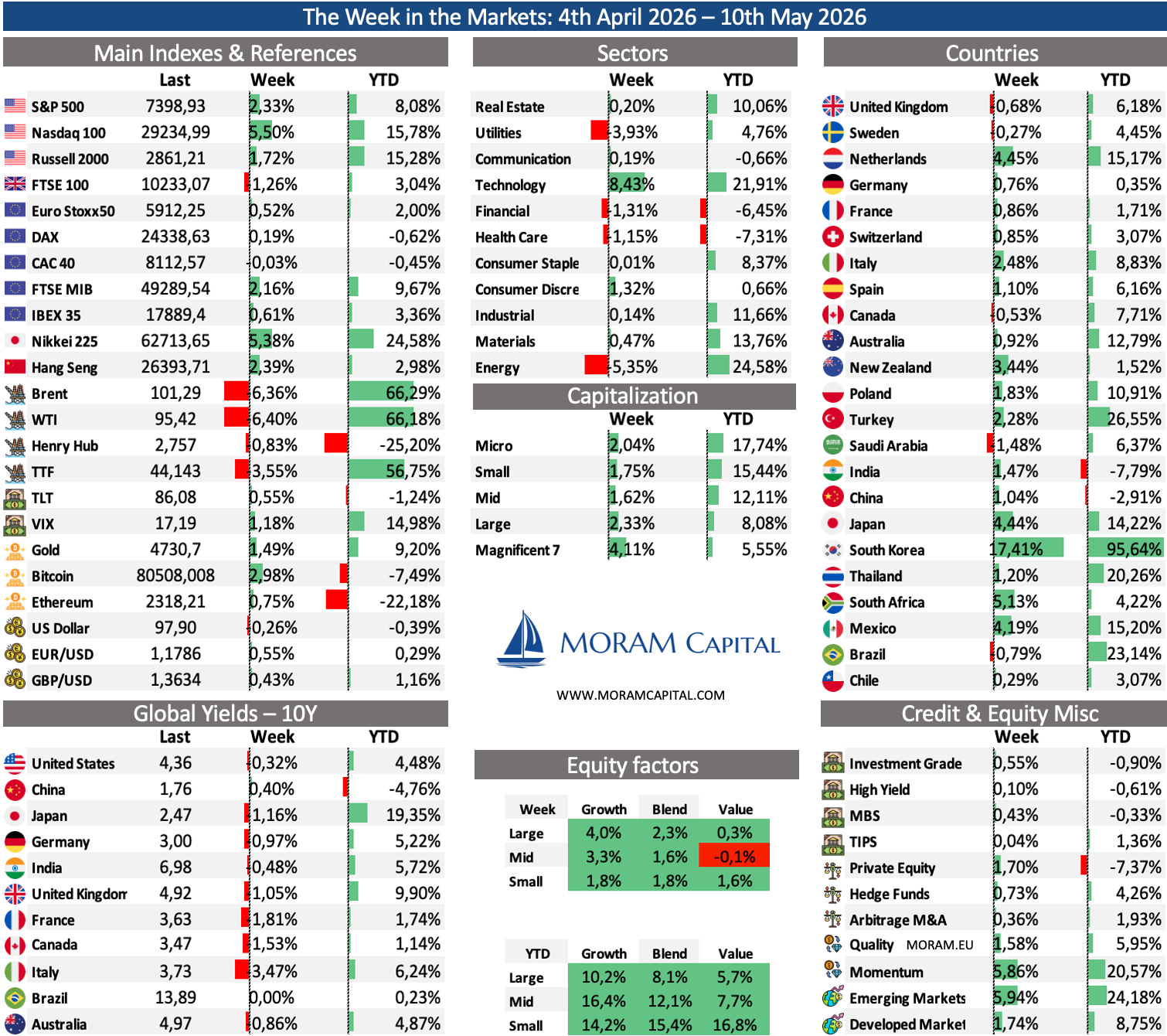

The Week in the Markets

A week of new all-time highs for the S&P 500, Nasdaq 100 and Russell 2000, with US equities continuing to separate from most global markets, Japan and South Korea aside. The move has been led by technology, the semiconductor trade and the recovery in the Magnificent 7, which are now up c.26% from the March 30 market low. The SOXX index is up 64% YTD.

The three main drivers behind this week’s move were clear: a very strong 1Q26 earnings season, with 84% of S&P 500 companies beating EPS estimates; macro data that came in better than feared, particularly on the labor market; and positive headlines around a potential end to the Middle East war, even if the credibility of those headlines remains highly questionable.

1) Earnings season

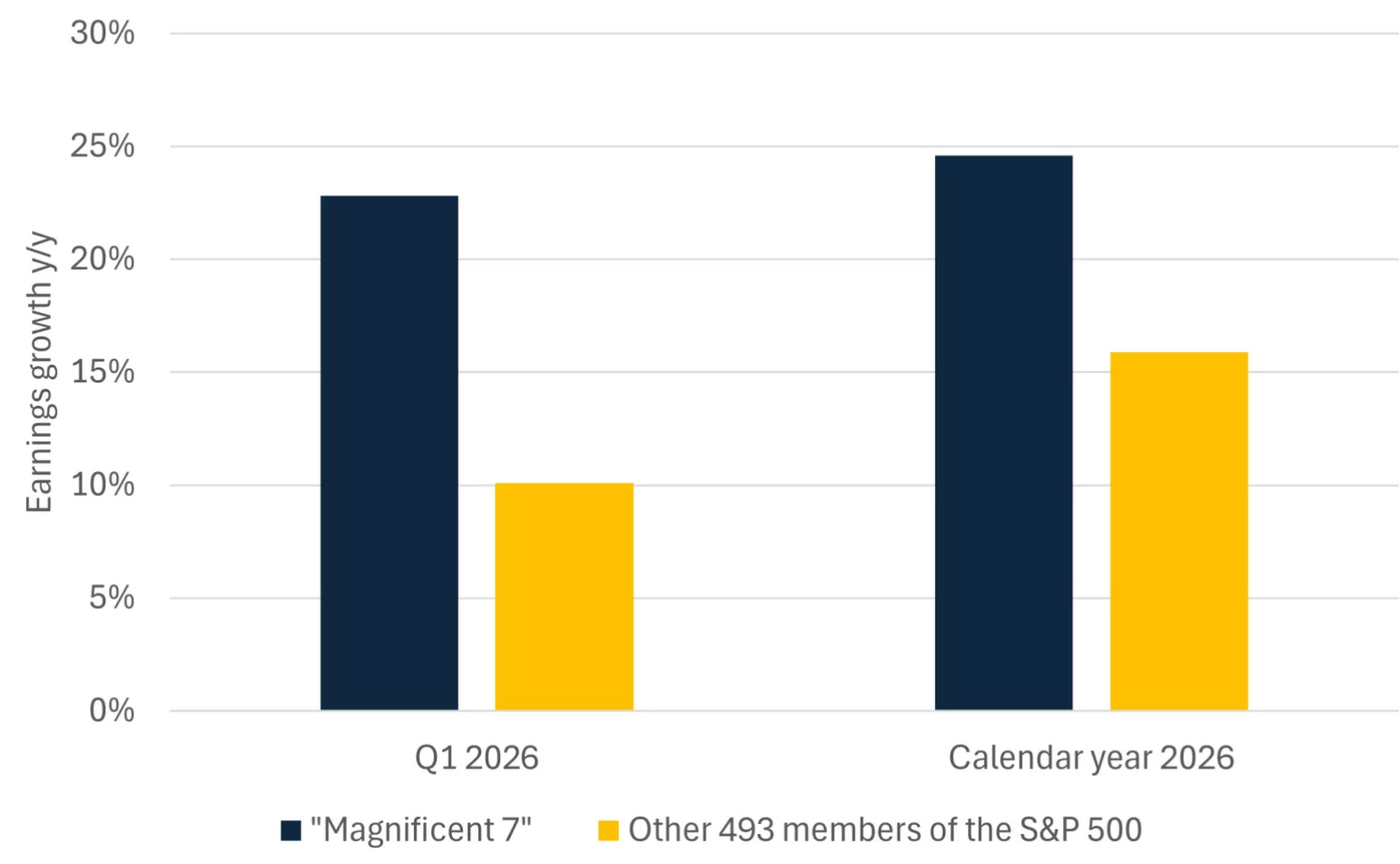

Earnings were again the main support for the market this week, particularly in technology and semiconductors. 1Q26 season continues to deliver: 84% of S&P 500 reporters have beaten EPS estimates, with 89% of the index already reported - the highest hit rate since 2Q21. Blended earnings growth is tracking close to 28%, the strongest since 4Q21. Ten of eleven sectors are reporting positive YoY earnings growth, with seven in double digits. The forward 12-month P/E now stands at 21.0x, above both the five- and ten-year averages.

The oil shock is only partly visible in these numbers, with the move in crude coming late in the quarter. Still, the data are useful: corporate profitability entered the shock from a position of strength, and that should provide some cushion unless oil moves materially higher from here.

Tech remains the clearest expression of that strength. The AI investment cycle continues to support earnings momentum, and semiconductors have been the main winner so far.

2) Macro

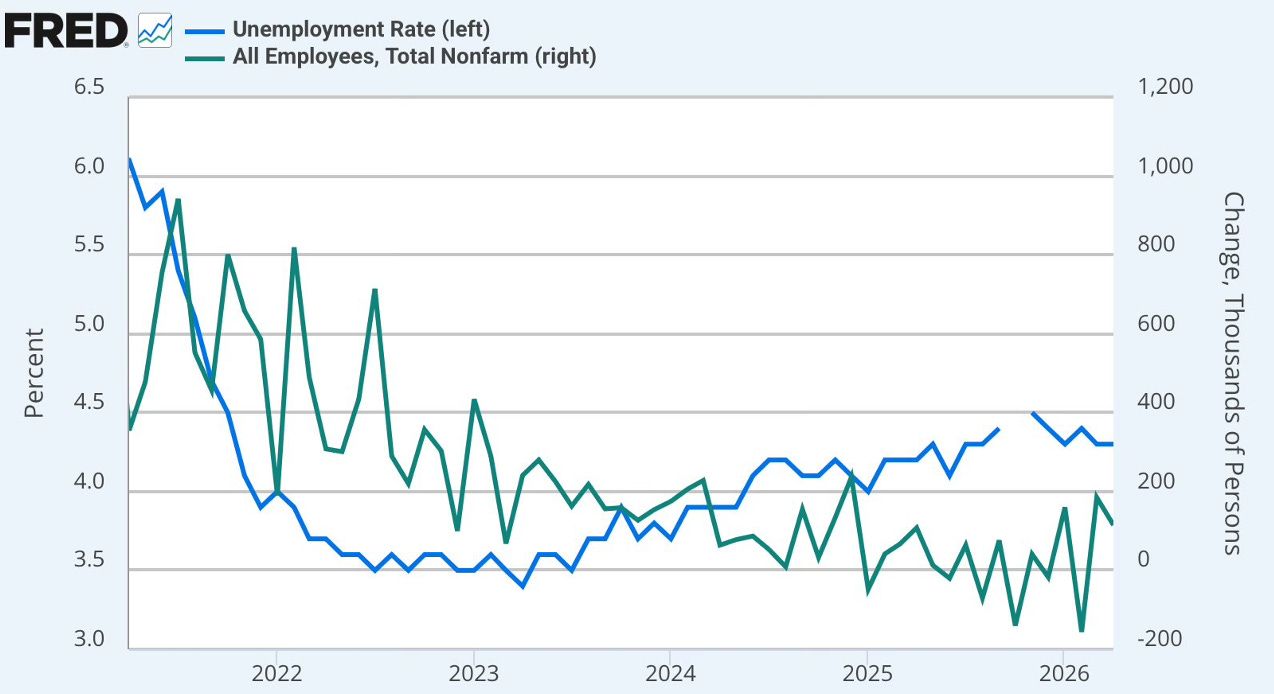

The main macro support this week came from the labor market. April payrolls rose by 115k, well above the 55k expected, while unemployment held at 4.3%. Wage growth also cooled to 0.2% MoM and 3.6% YoY, which is the important part in the current environment: higher energy prices are not yet feeding into wages. For equities, this is a good mix - the labor market is not breaking, but it is not hot enough to force the Fed into a more hawkish stance.

This is relevant because labor was one of the main concerns coming into 2026, after a very weak hiring backdrop in 2025. The latest data look better: private job gains have rebounded, hiring appears broader across sectors, claims remain low and households are reporting slightly better conditions to find work. The Fed still held rates at 3.50%-3.75%, and the transition from Powell to Warsh adds policy uncertainty, but this week’s macro message was simpler: growth is holding up better than feared, while the wage channel is not yet amplifying the oil shock.

3) Middle East

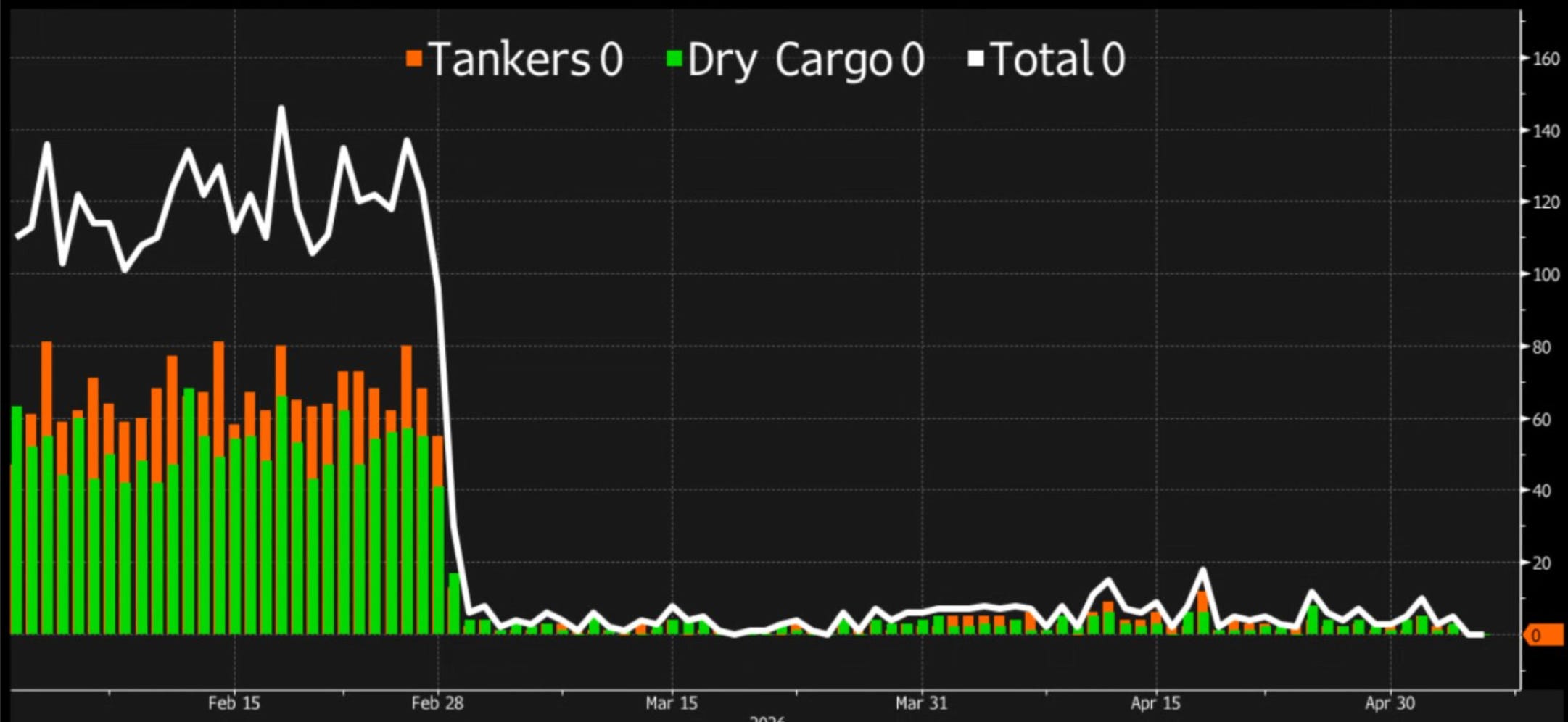

Another week, another Axios report pointing to a possible end to the Iran war. Oil sold off aggressively, equities rallied to fresh highs and the market once again treated the headline as a meaningful reduction in tail risk. The timing also raised eyebrows, with well-timed crude short positions reportedly opened shortly before publication of the story and closed shortly after the move lower in oil.

We still think markets are becoming too complacent around the physical impact of the conflict. Even if a diplomatic solution is eventually reached, inventories have already tightened materially, shipping through Hormuz remains under pressure and several banks - including Goldman - continue to assume disruptions extending well into 2H26. In our view, equity markets are focusing on the removal of the “peak fear premium” in oil, while largely ignoring the lagged impact that sustained inventory draws and supply disruptions could still have on inflation and growth over the coming quarters.

The Week Ahead

Next week is much less macro-defining than the recent mega-cap-heavy calendar, but still relevant for several high-beta areas of the market. The focus shifts toward AI infrastructure, semis, crypto-linked equities, fintech, China tech and energy-related names.

AI infrastructure / semis (Applied Materials, Cisco, Oklo) - This remains the most important part of the calendar. The focus will be on semiconductor equipment demand, networking spend linked to AI datacenters and whether the power/nuclear theme continues attracting capital after the recent rally in AI infrastructure names.

Fintech (Circle, Nu, Klarna) - Useful read on stablecoin activity, digital banking, consumer credit and broader risk appetite. This group should help show whether liquidity and speculative appetite remain supportive for fintech and crypto-linked equities.

China / online platforms (Alibaba, Sea, Wix) - The focus will be on whether China tech stabilisation is becoming more fundamental rather than policy-driven, while Sea and Wix should provide a cleaner read on online spending, software demand and SME activity.

Energy / materials (Constellation Energy, Barrick, NextDecade) - Energy and materials names will be judged on cash flow, commodity price realisation and project execution. Constellation and NextDecade are also relevant for the broader AI power demand and LNG infrastructure narratives.

Updated Equity Research - Kosmos Energy, Sanlorenzo, Excelerate Energy

Today we update our view on three very different businesses currently trading through periods where market perception and underlying fundamentals are diverging.

For each company, we review the latest results, operating trends, balance-sheet evolution, capital allocation and updated valuation. More importantly, we focus on the variables that are actually driving the equity story - balance-sheet evolution, cash generation, operating leverage and whether the current setup is structurally improving or simply benefiting from short-term conditions.

Kosmos Energy - Highly leveraged Oil & Gas producer has just reported its 1Q26 results. We analyse whether the rise in the share price already reflects all of the improving operations, higher oil prices, and lower capex intensity, whether there is still upside left, or whether the investment case is starting to become quite risky.

Sanlorenzo - One of the leading players in the global luxury yacht industry, with strong brand positioning and backlog visibility, in a market now facing softer industry demand after several years of exceptional conditions.

Excelerate Energy - The world’s largest dedicated FSRU operator, positioned around long-duration LNG infrastructure contracts and the growing global need for regasification capacity.

Note: We leave the link to our latest analysis of each of them. (In the Portfolio Management section, we talk about them weekly; we’ve started adding these sections to the website so they can be found more quickly.)

Sanlorenzo

Sanlorenzo is one of the leading companies in the global luxury yacht industry. Founded in 1958, the group historically built its reputation in the 30-40 metre yacht segment, where it has been one of the global reference players for more than a decade. However, Sanlorenzo as it exists today cannot be understood without Massimo Perotti, its current CEO and controlling shareholder, who acquired the company in 2005 and transformed it into a much broader luxury yachting platform.

Since Perotti’s acquisition, the transformation has been substantial. Revenue has grown from roughly €40MM at the time of acquisition to €960MM of Net Revenues New Yachts in 2025, implying a CAGR of approximately 17% over two decades. The company opened its Viareggio shipyard in 2007 for larger superyachts, expanded the traditional yacht business through the SD, SX and SP ranges, built Bluegame into a differentiated sport and chase boat brand, and more recently entered sailing yachts through the acquisition of Nautor Swan.

The industry backdrop has changed materially since the post-pandemic peak. Order intake across the sector has normalised, demand visibility is lower, and investors have become more cautious on the entire luxury yacht space. Sanlorenzo listed in Milan in December 2019 at €16/share, with a market capitalisation slightly above €500MM; today, the company has a market cap of roughly €1.2Bn, after having grown EBITDA to ~€181MM in 2025.

This is precisely why the distinction between companies matters more now than it did during the boom years. Sanlorenzo, The Italian Sea Group and Ferretti are often grouped together by the market, but their business mix, backlog quality, balance-sheet position and execution profiles are materially different. The sector is softer, but not all companies enter this phase with the same starting point.

Today, we review Sanlorenzo’s latest results, order intake, backlog, financial position, updated DCF valuation with the new 2026-2028 strategic plan… The key question is not whether the industry is softer - it clearly is - but whether Sanlorenzo’s current fundamentals and medium-term targets remain credible under a more normalised demand environment.