Campari - Initial Equity Research

The opportunity to own Aperol, Campari, Espolòn, Appleton, Wild Turkey... at liquidation price

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Campari - Full analysis of Campari, one of the world's leading premium spirits manufacturers (, which has dropped 60% in the last 18 months due to a mix of sector headwinds and internal setbacks. We analyse each of its brands and individual comparison with Diageo, Pernod Ricard... We also explain its business model, marketing strategy, capital structure, economics, valuation…. Downloadable spreadsheet with tons of information used for this analysis.

One of the most detailed analyses we have done in these 5 years.

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios

Investor Resources

Data Center Update

Financial model Updates

Nota: Toda esta publicación está disponible en Español en nuestra web

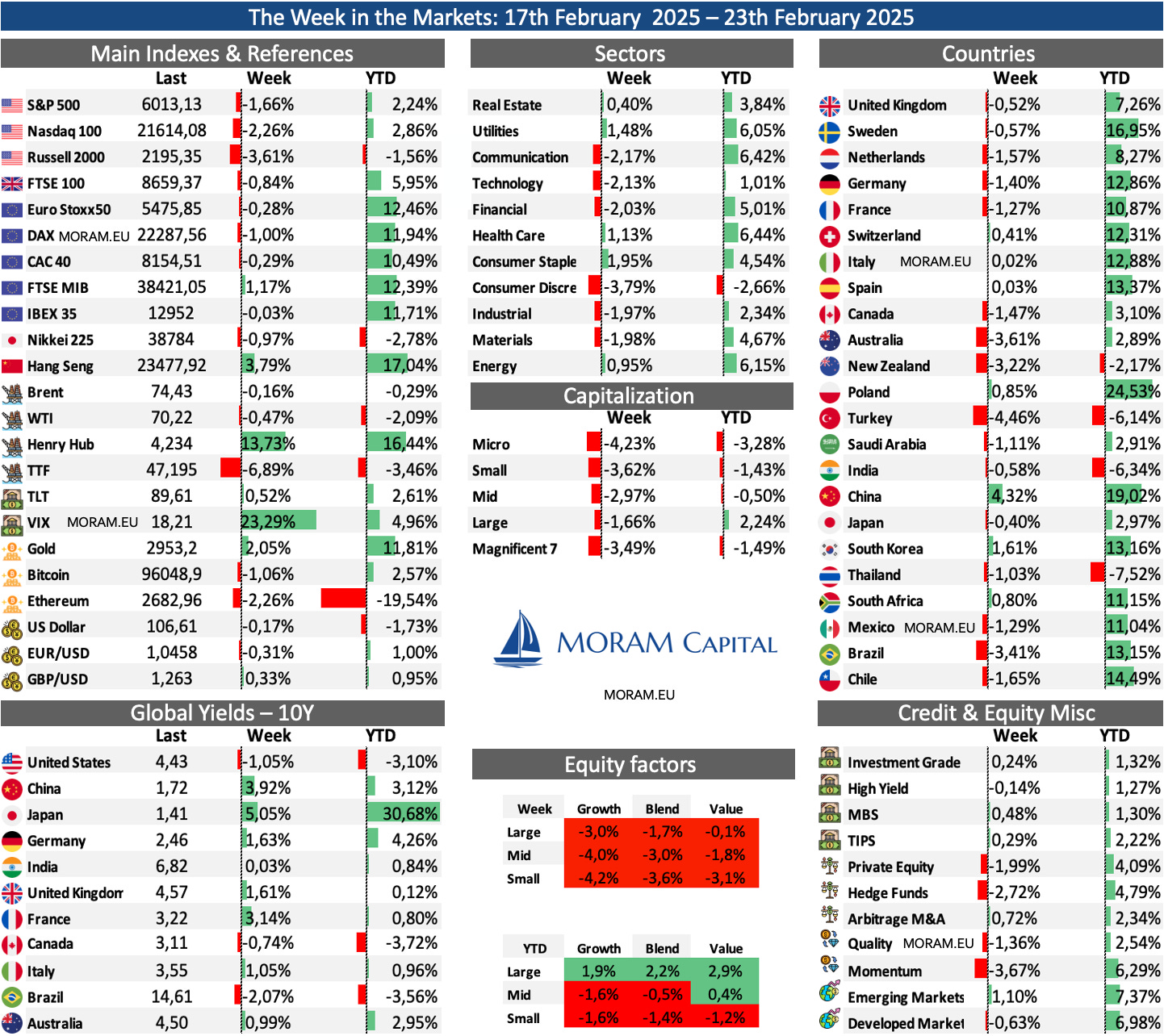

The Week in the Markets

Summary

The week started strong, pushing the S&P 500 to all-time highs on Wednesday, but then sharply reversed downward following Trump’s comments on tariffs, Walmart’s earnings, and Friday’s macroeconomic data. It’s also important to note that yesterday was a monthly options expiration Friday, which always adds volatility.

The biggest losses of the week were once again in the U.S. (notably, the gap between the U.S. and Europe in these first weeks of the year is becoming significant—this had to happen at least for one year…). In terms of market capitalization, an interesting trend emerged: the worst performers of the week were both small caps (Russell 2000) and the "Mag 7" (Tesla, Amazon, Netflix, and Meta all dropped more than 7% this week), with the latter now turning negative YTD. In fact, as seen in the equity factors chart, small caps have now clearly underperformed year-to-date, entering negative territory compared to the rest.

China remains unstoppable—its benchmark index (Hang Seng), which started the year with a nearly 7% drop, is now the best-performing major index of 2025 after gaining another 4% this week (mainly thanks to Tech stocks - the release of Deep Seek has acted as an authentic catalyst.). Meanwhile, Europe saw slight declines, with only Italy and Spain closing the week in positive territory among the major economies.

Regarding commodities, oil fell for the fifth consecutive week, though only slightly, while Henry Hub and TTF gas prices moved in different directions (since the dependence on U.S. LNG exports, although impacted, has many more drivers than the potential end of the Ukraine-Russia war (which does have a tremendous impact on Europe). Cheniere, the global LNG benchmark, released its market outlook this week

Gold continues climbing to new record highs, having closed positive every week of 2025. Meanwhile, Bitcoin attempted to break above $100K during the week but ended nearly flat at the time of writing.

The VIX, once again and as we mentioned last week, rebounded sharply as soon as it dropped below 15—this is becoming an increasingly obvious trade for many traders in recent months.

Lastly, the dollar also closed slightly lower and has now fallen in five of the last six weeks. U.S. Treasuries remain below 4.5% despite rising after the Fed minutes and PMI data.

Macro highlights

FED Minutes

The most relevant part of the Fed minutes this Wednesday (which pushed the indices to all-time highs) was likely the following statement:

"Regarding the potential for significant swings in reserves over coming months related to debt ceiling dynamics, various participants noted that it may be appropriate to consider pausing or slowing balance sheet runoff until the resolution of this event."

This indicated that Quantitative Tightening could end by mid-2025, meaning the Fed may stop draining liquidity earlier than expected.

Although this does not inject liquidity into the market (i.e., Quantitative Easing), it is a positive liquidity event since the Fed was currently draining $55 billion worth of liquidity per month (this halts downward pressure on Fed liquidity and bank reserves).

Another key takeaway was that Fed officials believe strong January CPI suggests better/lower inflation prints for the rest of the year, rather than indicating that Q4 inflation was too low.

PMI

The Manufacturing PMI rose to 51.6 (est. 51.4; prev. 51.2)

Services PMI dropped to 49.7 (est. 53.0; prev. 52.9), marking its lowest level since early 2023.

The Composite PMI fell to 50.4 (est. 53.2; prev. 52.7).

Optimism for the coming year has declined from near three-year highs at the start of the year to one of the lowest levels since the pandemic. Businesses report widespread concerns about the impact of federal government policies, including spending cuts, tariffs, and geopolitical events.

These PMIs are from S&P Global, but the most important ones come from ISM, which are released at the beginning of the month.

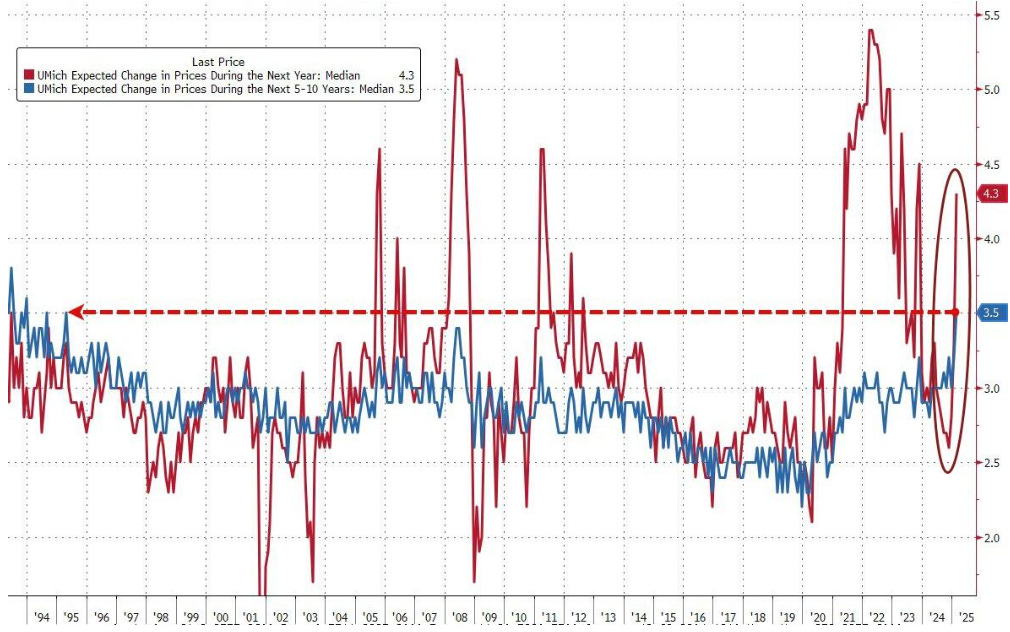

Index of Consumer Sentiment

The final University of Michigan consumer sentiment data came in worse than forecasts from a few weeks ago. The overall sentiment index dropped nearly 10% MoM to 64.7 (est. 67.8), with current conditions at 65.7 (est. 68.5) and expectations at 64.0 (est. 67.4).

All components of the index declined during the month, “led by a 19% plunge in buying conditions for durables, in large part due to fears that tariff-induced price increases are imminent,” according to Survey of Consumers Director Joanne Hsu

Inflation expectations remained unchanged at 4.3% for one year but rose to 3.5% (est. 3.3%) for the 5-10 year outlook. A key factor, as noted previously, is the strong political bias, with significant differences between Democrats and Republicans.

Housing data

Another alarming data point this week was the overall state of the housing market, which showed continued weakness and declining confidence among builders and buyers.

The Home Builder Confidence Index fell to 42 in February ( 47 in January), marking its lowest level in five months due to uncertainty around tariffs, high mortgage rates, and elevated housing costs.

Additionally, housing starts dropped nearly 10% in January to a seasonally adjusted annual rate of 1.37 MM, significantly below expectations. Existing home sales also declined, and homebuilder stocks hit 52-week lows, reflecting the overall weakness in the sector.

Interesting Data about markets this week & YTD

Earning Season 1Q25

The highlights of this week, which ends today, have been Walmart's results (and its weak guidance for 2025, which seemed to drive broader investor concerns regarding consumer spending and the health of the overall economy).

On our side, Cheniere reported good results and shared several highlights regarding the LNG market.

This week, Domino’s, HIMS, CAVA, NVIDIA, ABInBev will report results, as well as many companies from our investment universe, whose results we will discuss daily via the chat/express article for any relevant updates: Golar LNG, Unidata, Ferretti, Solaria, Gogo, Excelerate Energy, Intred, Vysarn..

Initial Equity Research: Davide Campari-Milano

Introduction

Campari is the sixth-largest player worldwide in the global premium spirits industry. Among its more than 20 brands, Campari, SKYY Vodka, Grand Marnier, Courvoisier or the emerging Espolón tequila or its star brand, Aperol, stand out.

Since its IPO in 2001 it has managed to multiply its revenues and EBITDA 6x (Revenues 494 to €3Bn, EBITDA 105 to €0.65Bn) as a result of a strategy that has combined the acquisition of more than 30 companies since 1995 and its organic growth with brands such as Aperol going from a turnover of just €25 million in 2003 (acquisition) to more than €700MM today. or Tequila Espolón, which since 2009 (acquisition) has gone from invoicing just €10MM to almost €300MM today.

However, Campari's last 18 months have been very complicated, not only with the contraction in demand that the entire sector is suffering but also with the farewell to its emblematic CEO (Kunze-Concewitz) who had been in his position since 2007 (and who, as we will see later, together with the founder of Campari and his son Davide, had become the third most important in the history of this brand), with the resignation of his successor (just 6 months after starting in office), with the acquisition of Courvoisier for almost €1.3Bn (which today, seems clearly surpassed) or with some scandals surrounding the Family Office of its Chairman, Luca Garavoglia (who is taking advantage of the situation by buying millions of shares)

All this has led to a 60% drop in the share price in this period of time, leaving it at a price of 14x EV/EBITDA, something that has not happened since 2015. This multiple represents a slight premium over its peers Diageo, Pernod Ricard... will present worse numbers than in 2023, while Campari thanks in large part to its Aperol and Espolón brands) continues to grow in sales in 2024 and maintain its EBITDA compared to 2023.

Today we present one of our most in-depth analysis in which we have been working since November. Our objective is to identify if we are facing a historic investment opportunity or if the fall and rerating is justified based on aspects that are not seen at first glance.

We cover:

Explanation of the Beverage producing business and the distinctions between the processes and economics of the different types of alcohol.

Detailed analysis of Campari’s main brands, strategy, and business model (Marketing, distribution, M&A,...)

Comparative analysis (for each beverage brand) with its main competitors (Diageo, Pernod Ricard,...) in terms of growth, economics,…

Detailed analysis of its finances, debt, and capital allocation.

Valuation and Spreadsheet with all the information used in this analysis (tons of data, not only of Campari but its peers)

Honestly, a masterpiece.