The Italian Sea Group, Sanlorenzo & Ferretti

Superyachts Industry Review

Hi there, we hope you had a fantastic week !

Please find this brief summary of the topics we are covering today

The Week in the Markets

Our weekly summary with the best charts to understand what happened in the markets in 1 minute, along with explanations for those who want to dive deeper.

Equities, Bonds, Currencies, Alternative Assets, Macro Data, company commentaries, Earnings Season, and much more!

Equity Research

Sanlorenzo - Italian luxury superyachts builder and sector leader that has reported very strong results and ambitious future plans. We review the company’s situation and update the valuation model after recently sharing with you the updated thesis (both in written and PPT versions). A gem trading at 6x EV/EBITDA.

The Italian Sea Group - Italian luxury megayacht builder that, despite the issues with Bayesian and the lack of new large-vessel orders, has delivered a solid quarter and is currently trading at less than 5x EV/EBITDA — despite having quadrupled its revenues over the past five years and improved its EBITDA margin to nearly 18%.

New Fortress Energy - Liquidation game. Analysis of the current situation and the value of its assets ahead of the imminent end of the company (chapter two of what we already anticipated five weeks ago here

Together with all the analyses, we’re sharing a downloadable valuation spreadsheet for you to use

Portfolio Management

Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios.

Investor Resources

Data Center Update - Adding Insider Transactions Monitor & Option Calculator

Financial model Updates

Nota: Toda esta publicación está disponible en Español en nuestra web

Disclaimer: This publication is for educational purposes only and should not be taken or considered as investment advice under any circumstances. Please consult with your financial advisor before making any investment decisions.

The Week in the Markets

Summary

A very good week for the markets, thanks in large part to the good news that started the week: a trade agreement between the US and China and a drastic reduction of tariffs for 90 days, which has brought the S&P 500 to less than 5% from its historical highs, marking another V-shaped recovery like the one we saw during Covid.

The best performers of the week – returning to the usual pattern of recent years – were the Mag7, which rose almost 10%, led by Tesla and NVIDIA, which gained 17% and 16%, respectively.

By sector, beyond Consumer Discretionary and Tech, boosted by those two giants, we see a strong rotation into more cyclical sectors, to the detriment of more conservative ones like Health Care and Utilities. To these we add Real Estate, which, with 10-year Treasury yields rebounding some days this week even above 4.5%, makes it hard to be optimistic.

By market cap, as shown in the YTD chart, the story of recent years repeats itself again and in general — although it’s true that for these comparisons the Russell 2000 may not be the best reference due to the index's composition and the number of zombie companies it contains — large caps are already in positive territory this turbulent year, while small caps remain deep in negative territory. Stock picking becomes crucial in these kinds of market environments…

Other relevant news of the week included President Trump’s tour of the Middle East and agreements with Saudi Arabia to purchase large amounts of advanced artificial intelligence chips from U.S. companies (which also helped NVIDIA and the markets), as well as investment commitments from Qatar.

Oil has moved up slightly (a thermometer for recession prospects, which have decreased this week with the tariff truce), and as usual in weeks of market gains, the VIX is down (now at $17, take note), and gold has retreated more than 4%(selling of safe-haven assets and rotation into higher-risk (and beta) assets when the market rises).

The villain of this otherwise nice story is undoubtedly the 10Y Treasury yields, which have closed near 4.50%, and this is a major headache for the U.S.'s debt refinancing plans (between April and June they have to refinance $6 trillion in debt).

With the market already closed this Friday, Moody's downgraded U.S. credit from AAA to AA for the first time in history, although for now it's not having much of an impact (in the past, similar moves from competitors led to drops of 5 to 10%) in the futures market over the weekend. We’ll see tomorrow.

This coming week is very quiet in terms of macro data and no major companies are reporting results, so the focus will likely be on U.S. debt and tariff negotiations.

Macro highlights

US CPI

April inflation data — the first month with new tariffs — came in lower than expected. So far, there's no sign of the tariffs affecting prices.

Headline CPI rose 0.22% MoM, bringing the annual rate to 2.33%, the lowest since April 2021 in four years.

Core CPI rose 0.24% MoM, keeping the annual rate at 2.78%, also the lowest in four years

Component breakdown:

Core goods prices rose 0.06% in April (from -0.09% in March), with annual inflation turning positive at +0.13%.

Shelter costs rose 0.33% MoM (+3.7% YoY) — still showing a moderating trend.

Core services excluding shelter rose 0.21% MoM (+2.8% YoY).

Housing costs accounted for over half the total monthly increase.

Energy prices rose 0.7%, driven by natural gas and electricity, offsetting lower gasoline prices.

Food prices fell 0.1%, with a 0.4% drop in grocery prices outweighing a 0.4% rise in dining out. Egg prices plunged 12.7%, the largest monthly drop since 1984.

Other declines: airfares, used vehicles, communications, and clothing.

Bottom line: Despite sharp tariff hikes in April, price changes were moderate. The deflation in goods seems to have stalled — after playing a big role in curbing inflation over the past two years — while disinflation in services, including both housing and non-housing, has continued steadily.

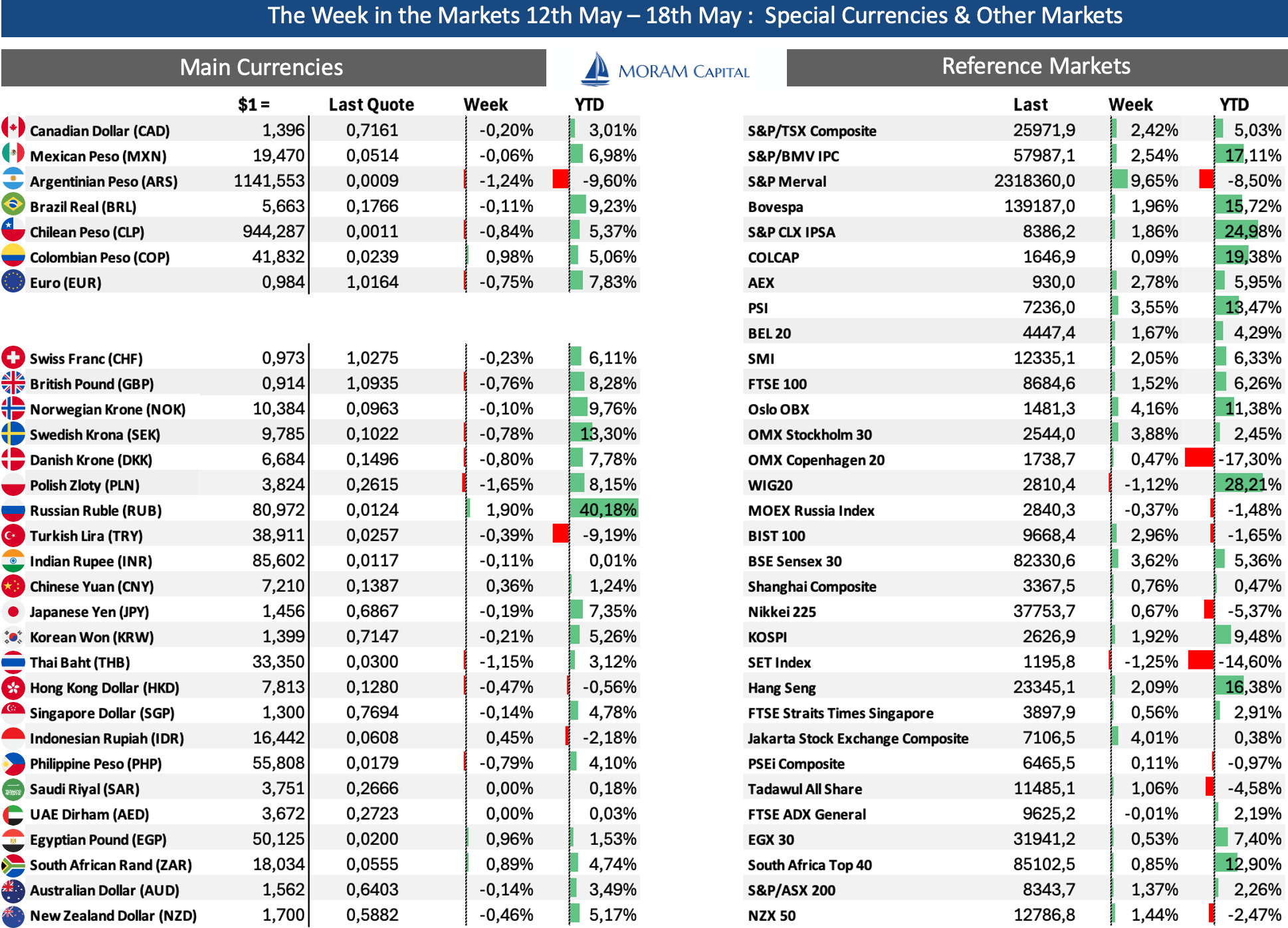

Interesting Data about markets this week & YTD

The main currencies have fallen this week against the dollar, which has been significantly strengthened by the news of investments in the U.S. resulting from Trump’s tour of the Middle East and the trade progress with China, whose currency has also been strongly boosted.

As for stock indices, it was a very good week overall, but particularly noteworthy is the Argentine stock market, which has recovered nearly 10% this week.

Expectations for Fed rate cuts have completely cooled down in the last two weeks, coinciding with the market rallies. If we look at inflation data, it’s actually hard to understand why they wouldn’t cut rates; however, if we look at Trueflation, which uses nowcasting techniques, it seems to have been rising these past few days. What seems certain is that Trump will keep applying pressure, and Powell, apparently, is not going to be intimidated.

Earning Season 2Q25

A very quiet week in terms of company reports, both in the overall market — where practically only NVIDIA remains among the big names for next week — and in our portfolio specifically, as the Golar report originally scheduled for this week has been postponed to next week.

Superyachts Industry Review

This week, the three publicly traded superyacht companies reported their results and despite uncertainty, they continued to grow and increase margins. The superyacht thesis, now almost four years since the TISG IPO that marked the beginning of our coverage of the sector - guide to the industry - , was quite simple and based on three factors:

Over the last decade (partly due to monetary expansion), the number of ultra-rich individuals had grown much faster than the number of megayachts (largely due to capacity limitations).

The target audience for these yachts is unaffected by economic crises—in fact, many of them pay for the yachts in cash without financing. Therefore, in a potential economic slowdown, they would be much less impacted than buyers of recreational boats (publicly traded US manufacturers and, although larger, the three French catamaran and monohull companies).

COVID-19 triggered a trend shift, increasing the interest of wealthy individuals in owning their own superyacht.

It is well known that the main fear in recent months (and the reason why share prices have dropped more than 30%) is the concern that the three companies might face the same issues as the <24m boat manufacturers, where the market is experiencing significant problems (cases we discussed in the industry guide covering Malibu Boats, Mastercraft, Brunswick, Marine Products… or in more detail, the French companies Catana and Beneteau). However, as the quarters have gone by (and with major differences between companies), revenues and margins have continued to rise, and order intake has managed to hold up.

Today, we review these companies individually and focus on whether the worst is over for the industry or if there are still challenges ahead. Specifically, looking at Sanlorenzo and The Italian Sea Group, we see that their paths are diverging.

Note: Equity reports (Italian Superyacht companies) and updates (on bio)

The Italian Sea Group

The Italian Sea Group is an Italian luxury megayacht builder and one of the companies we have dedicated the most time to in recent years. Its history, as we know it today, began in 2009 when Giovanni Constantino, founder, CEO, and majority shareholder of TISG (53.6% ownership), purchased the historic Italian yachting brand Tecnomar and, two years later, Admiral, which is now the group’s flagship brand. At the end of 2012, Tecnomar acquired NCA, giving birth to the holding company The Italian Sea Group and starting their refit activities (later in 2015).

2021 was a landmark year for the company. They went public raising 45 million euros which they used to acquire the historic Perini Navi shipping company, which was in bankruptcy. Thereby obtaining the two brands owned by the company (Perini Navi and Pichhiotti) and the facilities in Viareggio and La Spezia, which together with the investments in the Marina di Carrara shipyard (where until that moment they have carried out all their operations) have allowed them to double their production capacity. Also, during the same year, they launched the first of the 63 yachts in partnership with Lamborghini and signed a deal with Armani to design yachts over 72 meters.

The company’s evolution has been exceptional. Sales and profits have grown significantly, from €23.6 million in sales in 2009 to over €400 million in 2024 (CAGR = 21%), with an acceleration in growth over the past five years, during which it has been by far the best-performing company in the sector.

The current situation is quite different, and some of the optimism from recent years has evaporated. The widespread headwinds in the industry and TISG’s particular situation due to the sinking of the yacht Bayesian this summer (a Perini Navi yacht built before its acquisition, but one that generated headlines in The New York Times and comments from former employees) are delaying order intake more than usual and casting doubt on the fulfillment of this year’s guidance.

This quarter, the positive surprise has been the extension of existing orders (not the sale of large yachts, which have not been announced for a year now), which has allowed for only a minimal drop in the net backlog. But now, the death of a diver just as the salvage operation began will likely delay conclusions further and prolong uncertainty, especially as new information emerges that directly points to the yacht’s design.

Despite the rebound over the past month, The Italian Sea Group is currently trading at less than 5x EV/EBITDA and has lost more than 40% of its market capitalization in the last 12 months.

Today we analyze the situation of both The Italian Sea Group and Sanlorenzo, update the DCF models and valuations of both companies, and give our opinion on the state of the industry, including comparisons with Ferretti and the French players.