To be or not to be - New Fortress Energy situation & Excelerate Energy

Deep analysis of a key moment for New Fortress & Analysis of LNG industry Results

Hi there!

The Week in the Markets: One pager with a concise summary of the markets plus the highlights of the week regarding macroeconomy, liquidity, commodities, Middle East, Bitcoin, Earnings season…

Excelerate Energy: Analysis of the results and update of the thesis for this quasi-unknown natural gas infrastructure company, which is one of our great discoveries due to all the potential it has.

New Fortress Energy: Full review of the situation after the results, update of the guidance, and how the market lost patience. It is a rather critical analysis, with numbers in which we consider the different scenarios and position ourselves

Jack in the Box: 3Q24 results & investment thesis update (published this Monday)

Models / Spreadsheets updates (available on our website): Excelerate Energy, New Fortress Energy , Jack in the Box and ( Later this coming week : Cheniere Full House Resorts & GOGO)

Portfolio Management: Including updates on our 3-stage monitor, comments on several companies, and our macro views, along with their respective movements in both equities and all asset portfolios (

Data Center We continue working on our data center and we expect to release its v1 at the beginning of September. Already has 70+companies, and provides real-time information on everything related to them (press releases, earnings, earnings transcripts, insider trading, analyst recommendations, Historical income statement , BS, Operational cash Flows, Capex, buybacks, dividends... - individually reviewed by us).

The Week in the Markets

A highly eventful week dominated by volatility. The VIX, which surpassed 65 (the third time in the last 35 years it has reached this level), ended the week in negative territory. Despite significant drops at the start of the week, the major indices closed nearly flat on Friday; specifically, the S&P lost 0.04%, with small caps being the only segment that lagged behind.

In terms of equity factors, the week’s gains were driven primarily by large-cap growth stocks, continuing the trend where growth has significantly outperformed value.

Internationally (outside the U.S.), the week was marked by a slight increase in Japanese short-term interest rates (0.25%), which led to a partial unwinding of the carry trade. This strategy involves borrowing at near-zero interest rates in Japan and investing the funds in higher-yielding assets in the U.S. and other countries. The recent sharp rise in the yen made this trade less profitable, prompting many investors to exit their positions.

The 10-year bond yield recovered some ground last week as fears over a weakening labor market appeared to ease. A significant drop in U.S. jobless claims helped alleviate concerns, which had been intensified by weak U.S. manufacturing and employment data.

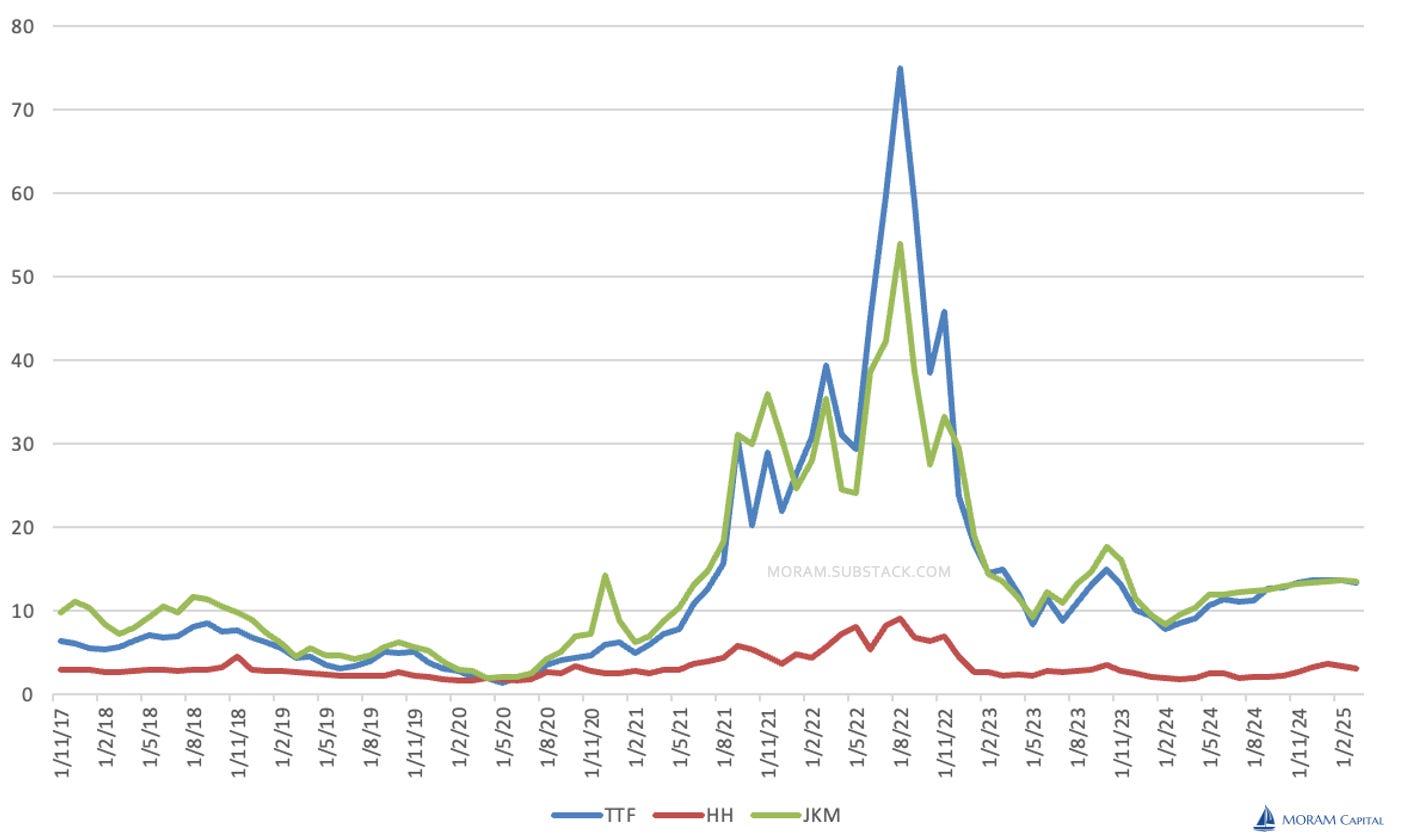

The highlight of the week was the performance of commodities, particularly European gas. The TTF/JKM - HH arbitrage has become quite profitable again (more details on this later). These increases were mainly due to the Ukrainian military capturing a key transit point for European gas imports via Russia (Sudzha), as well as high LNG demand from Asia due to the heatwave and some outages from major producers.

Data in $/MMBtu

Emerging markets had a strong week, led by Mexico and Brazil, while developed markets saw relatively modest gains.

Macro data

Very few macro events this week, aside from the ISM Services report (activity fell slightly in July to 55.5 from 56.0 in June but remained solidly in expansion territory—marking its best three-month growth period in two years), which provided some relief to the data from last Thursday and Friday.

A reassuring drop in weekly jobless claims on Thursday seemed partly responsible for a bounce-back rally, with the S&P 500 achieving its best daily gain since November 2022. Weekly claims decreased to 233,000 from an upwardly revised 250,000, although the number of continuing claims increased slightly by 6,000, reaching 1.875 million.

And a couple of images to illustrate the current situation:

Source Factset

Earning Season

A very intense week in terms of earnings presentations, with the most relevant aspect being the drop in New Fortress Energy, not just due to the results, but due to the loss of market confidence in the management and doubts about their liquidity in the coming quarters. Also, a very bad week for Airbnb, which, like other companies such as Disney, has reported softer travel demand, and Yum Brands referenced slowing sales at its KFC and Pizza Hut franchises.

This coming week, we have very few results, but they are from companies very relevant to us such as Golar LNG, Arcos Dorados, and Epsilon Energy. We will analyse all of them as they report and will share the information via Substack chat & email.

To be or not to be - New Fortress Energy situation & LNG industry results

Excelerate Energy 2Q24 Results

Very good results from Excelerate Energy and a new increase in Guidance. Plus the announcement of a deal in Vietnam and another that seems close in Alaska.

Financial results: Adjusted EBITDA of $89MM and Net Income of $33MM (an increase of $14MM compared to 1Q24 due to the impact of their dry dock in the previous quarter).

They are increasing the Guidance to $320-$340MM in Adjusted EBITDA. Growth Capex $70-80MM (most of which is allocated to the new FSRU for June 2026) and Maintenance Capex $50-60MM, totaling about $130MM in Capex.

Buybacks: In one year they have repurchased more than 1MM shares (in fact, just in 2Q24 they bought 674K shares at an average price of $16.27). They speak of opportunistic buybacks, so we think that the $30MM remaining from their $50MM buyback authorization will be used if there is a moment when the stock price returns to $16-$17, and not as actively at $19-$20, which seems to make perfect sense to us.

If we compare the results with the same quarter last year, there is a tremendous drop in Revenues but practically the same EBITDA (actually a bit higher this year). This is simply because before they had a ship in Brazil selling gas and not on a charter contract, so they recorded the gas sale but the COGS were also very high because they had to pay for the gas (they are not producers).

Let's take a detailed look at the progress over these three months and update the thesis, our calculations, and target price.

Thank you for reading! The rest of the article is for our premium subscribers. If you wish to become a premium subscriber and support our project, please do so through our website, where the prices are more attractive (we use the same gateway - Stripe, but we suffer lower commissions). Upon registration, you'll gain access to: